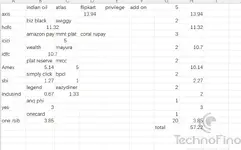

Hello everyone, one question! I have 9 credit cards: Axis IndianOil card (got in Feb 2023), HDFC Moneyback+ (May ‘23), OneCard (Jun ‘23), Amazon ICICI (Nov ‘23), SC Platinum Rewards (Feb ‘24), IndusInd Rupay & AU Bank Altura+ (both in Apr ‘24), and finally IFDC Millennia & Amex MRCC (both July 2024).

I’ve cut my expenses because of personal issues and as per my set budget, I intend to spend on MRCC, HDFC (for occasional offers), IDFC (I have a bank account there so it’s kinda easier, and I use its UPI), Amazon ICICI (I have Prime Shopping Edition), and OneCard (for looks). Plus all these have higher limit (7.5 Lacs combined).

Now the main question is, if I close the remaining CCs, will it impact my credit score in the long term? I want to close them because I read somewhere that we must not keep our Card Utilization zero and the minimum in the bill statement should be at least 1% of the credit limit of each card rather than zero.

If I consider that 1% tip, it means I’ll have to spend around ₹500 on each of the remaining cards just to avoid showing my utilization as zero, and it is not worth to spend ₹2-2.5k on those extra cards when I can spend that money on MRCC or Amazon for shopping, or even invest that money somewhere.

Basically you can tell me if I keep those cards unused (or usage not around 1% but less than that, i.e., around ₹100-200), will it impact my credit score negatively? Or closing the CCs would make more sense as I don’t really need those cards (I'm also considering their value or profit I'm getting) and closing them won’t impact my credit score for the longer run? I don’t think closing them earlier (<1 year) would make any significant impact.

An additional point: I talked to CC department of AU SFB credit card, and he told me that it’s a myth to use each one of our multiple cards every month because it’s the total CUR which impacts credit score and not the CUR of individual card. This means if I only use my 2-3 cards and the total CUR is between 3-30% then I’m all set because CCs are for “emergency use” and there’s no compulsion on us to use them every month—and thus I can keep the remaining cards unused.

P.S.- I'm not authorised to post this as question in the concerned forum so asked it here. Thanks for reading it till the end!