Ex: ABC Card

Statement Date: 20 (of every month)

Due Date: 10 (of every month)

Total Credit Limit of ABC Card - 20000

Cibil Reporting Date: 30 (of every month)

Current Date: 25

Due Amount: 10000 (as per statement)

-------------

So, Current Utilization Ratio: 50% which ABC Bank reports to Cibil on 30th of that month.

--------------

Few Points:

- One of the primary advantage of credit card is to utilize interest free amount from that ABC Bank Credit Card, and at the same time accumulate some interest on our XYZ Savings Account till that (due date - 5) (adjusted if any issues with bill payment platforms) for that amount.

- One of the factor that affects credit score majorly is Credit Utilization Ratio which can increase or limit new cards/loans on our account.

-----------

If you clear your dues by 29th, then bank reports your utilization ratio as - 0%

If you paid after 30th, then bank reports your utilization ratio as - 50%

(Note: 2nd condition has less impact if you have longer credit history)

---------

Options:

Always pay before due date with any case.

- If your CUR crosses more than 50% frequently, try to pay before month end/bill generation date (depends on bank).

- If CUR not much, then keep that amount in your savings account, increase your MAB then pay of before due date.

- Follow both to reduce CUR and to get some interest in Savings.

-----------

Hope you got some idea. Cibil behavior for score is unknown, above based on internet and personal observation. We can always pay off as soon as paid for that product, if there is some doubt that the amount may not be available at the month end (give high priority to credit card bills or any loan bills).

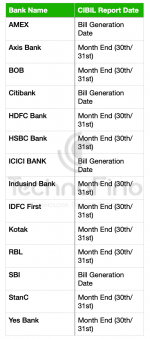

More information: