Extrovert🌃

TF Select

As i wasn't eligible for any Credit cards in past because of my age and No income proof, i had to choose the path of NBFC for just the sake of building something out of -1 or 0 as i had seen my relations go through how Imp CS is... so i had applied for the following

as i just got approved for Axis FK & Neo , i was wondering what to do with the above Personal/Consumer Durable Loan accounts. i'm currently focused on building Credit Score afresh as i might need it for auto or 10-15 years down the line Home Loan.

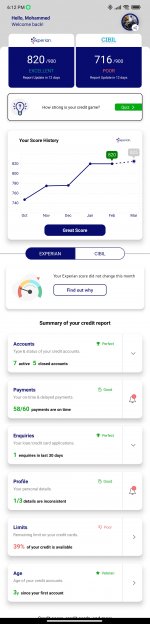

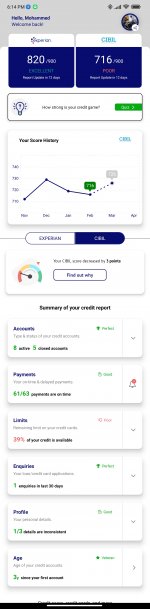

Score took a hit as i had applied for quite a few cards as i had just turned 21YO...

| Paytm Postpaid - 10k- Aditya Birla Finance & Clix Finance |

| LazyPay - 20k - Payu money |

| Zest Money - 40k - Ghalla Bhansali & Incred Finance |

| Flipkart PayLater - 40k - IDFC Bank |

| Freecharge PayLater - Axis Bank (Closed) |

| Amazon Pay later - Capital Float (Closed) (2 delayed emi at 1st COVID Wave) |

| Slice - 15k - Quadrillion Finance |

as i just got approved for Axis FK & Neo , i was wondering what to do with the above Personal/Consumer Durable Loan accounts. i'm currently focused on building Credit Score afresh as i might need it for auto or 10-15 years down the line Home Loan.

Score took a hit as i had applied for quite a few cards as i had just turned 21YO...

Attachments

![IMG_20220318_175448[645].jpg](/community/data/attachments/0/153-1509a88a149cc1eca6fdc992c76017ed.jpg?hash=FQmoihScwe)