RSDC pdf .Koi inn dono ki PDF file attach kar do yaha please.

I cannot access PDF file myself

Attachments

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

RSDC pdf .Koi inn dono ki PDF file attach kar do yaha please.

I cannot access PDF file myself

Used railway lounge on 18 February using canara rsdc at platform 1 new delhi and yes railway lounge was thereNever was there, I guess. Well not there now. See the above pdf

Okay my mistake. Did not know. Deleting previous comment.Used railway lounge on 18 February using canara rsdc at platform 1 new delhi and yes railway lounge was there

Railway lounge was better than airport lounge. I guess now there will be no railway lounge 😔.Okay my mistake. Did not know. Deleting previous comment.

Nowhere is it mentioned in the new circular. So maybe not anymore... 🥺Railway lounge was better than airport lounge. I guess now there will be no railway lounge 😔.

I agree with the private company aspect.

But 1275/lounge ain't true. Domestic lounges are provided en-block to banks at around 300. Even 2 lounges per quarter was not making them loss.

No, Rs1275 is not incorrect information.1275rs !!??? bewakuf bana rahe hai... har ek bank bulk mein uthata hai lounge entries aggregators ya directly lounge se in thousands or even lakhs... domestic lounge ki per entry.. 100-150 se jayda nahi padti inko... market trend chal raha hai.. lounge access limit krna... indirectly thik bhi hai...

No, Rs1275 is not incorrect information.

This news is from two years ago. Ankur Mittal had mentioned that banks pay ₹800-900.

If you don't know Ankur, he is the founder of CardInsider. He has considerable knowledge.

Even last year, he checked and found that banks pay ₹700 to ₹900 per customer.

Now, coming back to the ₹1275 cost—lounge costs vary depending on the airport and city tiers.

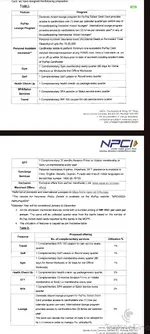

NPCI has also mentioned:

"The above price will be subject to change in case the merchant revises the same. The revised rates will be communicated to the member banks."

One more thing to consider: In the past few years, we’ve seen that most banks have set up their own lounge partnerships and discontinued card network lounges. Perhaps the reason for this is that card networks—whether RuPay, Visa, or Mastercard—charge slightly higher fees. Otherwise, why would banks feel the need to establish their own lounge tie-ups?

Applicable for select too? Didn't see it mentioned like thatSo now the minimum spend for Rupay Debit for lounge access will be only 10k in previous quarter. right??

The airport lounge access spend based limit is decided by banks, not NPCI.So the summary of the circular is that.

1) Bank need to pay 250 per card to NPCI, upto a utilisation of individual benefits as shown as (utilisation ratio). Beyond this utilisation limit (cap), bank needs to pay extra per usage to NPCI.

However the price tariff associated in Annexure A is at MRP. So we consumers would never know at what price it is bought by NPCI and being charged from the bank beyond the Utilisation Limit.

2) Lounge devalued to 1/Qtr without any spend limit. International lounge remains unchanged. Railway lounges not anymore I guess.

3) Banks might push for more RSDC, as for annual issuance more than 25k, bank will get rebate from the 250/- and additional tariff, starting from 20% to 80%. Hence more profit to the bank. So would not be surprised if the eligibility for RSDC would now be lowered.

Bhai apse railway lounge Kai bare mai pucha uska bhi kuch bataoThe airport lounge access spend based limit is decided by banks, not NPCI.

If banks want they can increase access from 1 lounge to 2 lounges per quarter or even reduce it to 0 lounges per quarter.

Of course, banks will have to bear the cost for it.

For some banks attracting customers solely through lounge access is their USP.

If they want, they can still offer 2 or 3 lounge visits per quarter on RuPay Select debit cards.

Hope they continue this.I believe the Amazon pay offer for RPDC will be decided later?

Am i right?

Can you share RPDC pdf alsoRSDC pdf .

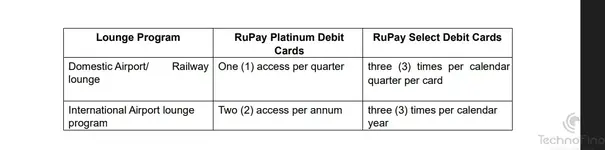

Arey ha, maine Platinum ka dhayan he nahi diya tha. 🤣🤣If I am reading correctly - for RuPay Platinum Debit Card Holders - 1 lounge access per calendar year. Earlier it was 1 lounge access per quarter. Huge Devaluation.

Same I checked in pdf for RPDC 1 lounge/yr domestic 1 and international 1If I am reading correctly - for RuPay Platinum Debit Card Holders - 1 lounge access per calendar year. Earlier it was 1 lounge access per quarter. Huge Devaluation.