silent.night

TF Buzz

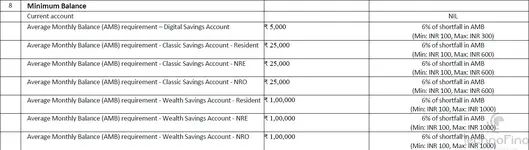

SBM Bank has been offering zero-balance "Wealth" accounts with a premium Visa Signature debit card offering features like global LoungeKey-based lounge access (3 per quarter, no spends criteria) and zero-forex international transactions. They are now introducing a minimum balance requirement. Here's the email I received stating there will be an AMB requirement of 1L starting from 1st Dec 2025 on the wealth savings account. The schedule of charges on their website details AMB for all of their account types. I'm not sure if they have been offering zero-balance for the other account types or how the change affects those.

I personally have found their debit card useful a few times. I once forgot to carry my Infinia's priority pass on a short international trip. I had not maintained any balance in my SBM account, but after I transferred around 4000, I was able to get access to a lounge. They deduct the full charge for the lounge access and then automatically refund the entire amount around 2-3 weeks later, like a pre-authorization on credit cards.

Another time my Infinia did not work on a fuel pump in Italy with HDFC SMSing me "This kind of transaction is not supported on your card". Luckily I had already transferred some money into the SBM account, so I could quickly use their debit card instead. Fuel pumps in Italy make a pre-auth for around 100 Euros and then settle the transaction based on the actual pumped amount a few days later. In this case too, the refund took around 3 weeks to be processed back to my SBM account. Two weeks into the wait, I had written to SBM's customer support. I'm not sure if that helped with the processing, and I didn't hear back from the bank aside from an automated confirmation email that my request has been received.

I'm still debating whether I should continue to maintain the account. I don't mind maintaining a small amount as AMB for a worry-free zero-forex debit card option aside from the Niyo cards. I suppose the lounge access is a feature that could justify the steep 1L AMB requirement, but given that I have other options for lounges, may not make sense for me to keep such a high amount with them. Also given their frail customer support and past run-ins with RBI regulators, it may not fully satisfy the "worry-free" criteria at 1L AMB.

I have Niyo's zero-forex debit cards, both SBM Bank and the newer DCB savings-account backed variants. However given they are an extra fintech layer on top of the banks, there's always a chance of changes and churn. For example their Equitas partnership has ended, with the bank discontinuing the zero-forex feature. The older current account-backed DCB card was also phased out and it took nearly a year after that for me to be able to apply for the newer variant online via the Niyo app.

I personally have found their debit card useful a few times. I once forgot to carry my Infinia's priority pass on a short international trip. I had not maintained any balance in my SBM account, but after I transferred around 4000, I was able to get access to a lounge. They deduct the full charge for the lounge access and then automatically refund the entire amount around 2-3 weeks later, like a pre-authorization on credit cards.

Another time my Infinia did not work on a fuel pump in Italy with HDFC SMSing me "This kind of transaction is not supported on your card". Luckily I had already transferred some money into the SBM account, so I could quickly use their debit card instead. Fuel pumps in Italy make a pre-auth for around 100 Euros and then settle the transaction based on the actual pumped amount a few days later. In this case too, the refund took around 3 weeks to be processed back to my SBM account. Two weeks into the wait, I had written to SBM's customer support. I'm not sure if that helped with the processing, and I didn't hear back from the bank aside from an automated confirmation email that my request has been received.

I'm still debating whether I should continue to maintain the account. I don't mind maintaining a small amount as AMB for a worry-free zero-forex debit card option aside from the Niyo cards. I suppose the lounge access is a feature that could justify the steep 1L AMB requirement, but given that I have other options for lounges, may not make sense for me to keep such a high amount with them. Also given their frail customer support and past run-ins with RBI regulators, it may not fully satisfy the "worry-free" criteria at 1L AMB.

I have Niyo's zero-forex debit cards, both SBM Bank and the newer DCB savings-account backed variants. However given they are an extra fintech layer on top of the banks, there's always a chance of changes and churn. For example their Equitas partnership has ended, with the bank discontinuing the zero-forex feature. The older current account-backed DCB card was also phased out and it took nearly a year after that for me to be able to apply for the newer variant online via the Niyo app.

Attachments