Credit cards were not very popular in India, at least until 2015. In the last few years, credit cards have become one of the preferred methods of digital payment. As you all know, India is the number one country in the world in terms of digital payments. More people are joining this digital payment revolution day by day. In January 2015, the total number of credit card users was 2,06,12,165 (Source: RBI Data). This number grew to 2,88,45,858, with approximately 83.33 lakhs credit cards added by the end of January, 2017. In January 2019, the total credit card users numbered 4,51,71,042, and by July 2023, it’s standing at 8,98,73,251, almost 9 crore credit cards. It is forecasted that this number might grow to 10 crore by the end of the current financial year.

Read this article on TF Community & Discuss with other members: https://www.technofino.in/community/threads/is-this-the-end-of-credit-card-business-in-india-for-foreign-banks.17400/

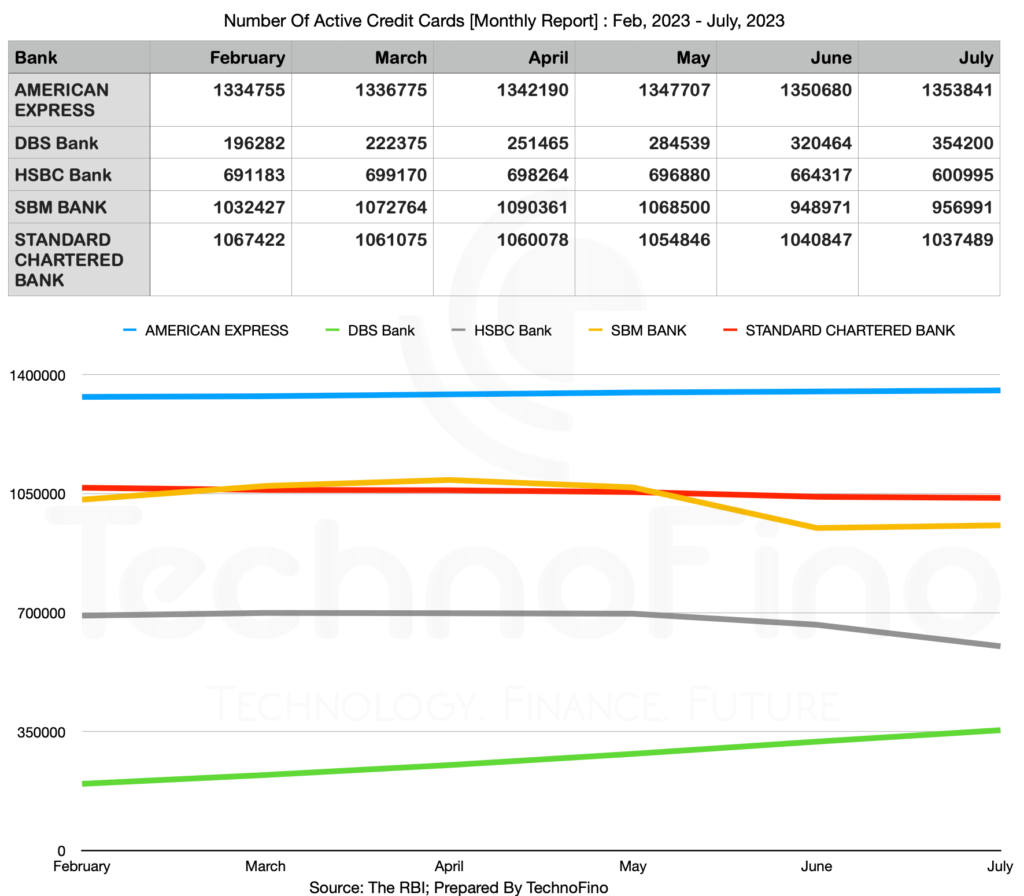

On the other hand, foreign banks are struggling with their credit card business. Big credit card companies and banks like American Express, HSBC, and Standard Chartered are all struggling in India. If we look at the last 6 months’ data, we can clearly understand that something is wrong with most foreign banks. Foreign banks have a history of struggling with their credit card business in India. In 2011, Deutsche Bank sold its credit card business to IndusInd Bank, and just two years later, in 2013, Barclays Bank sold its credit card business to Standard Chartered and Kotak Mahindra Bank. Same year, RBL Bank has acquired RBS credit card business in India. Recently, in 2022, CitiBank sold its Indian banking business, including the credit card portfolio, to Axis Bank.

So why are all these foreign banks leaving India or struggling?

Let’s examine the current numbers of foreign banks, and then we’ll try to understand the possible reasons for this.

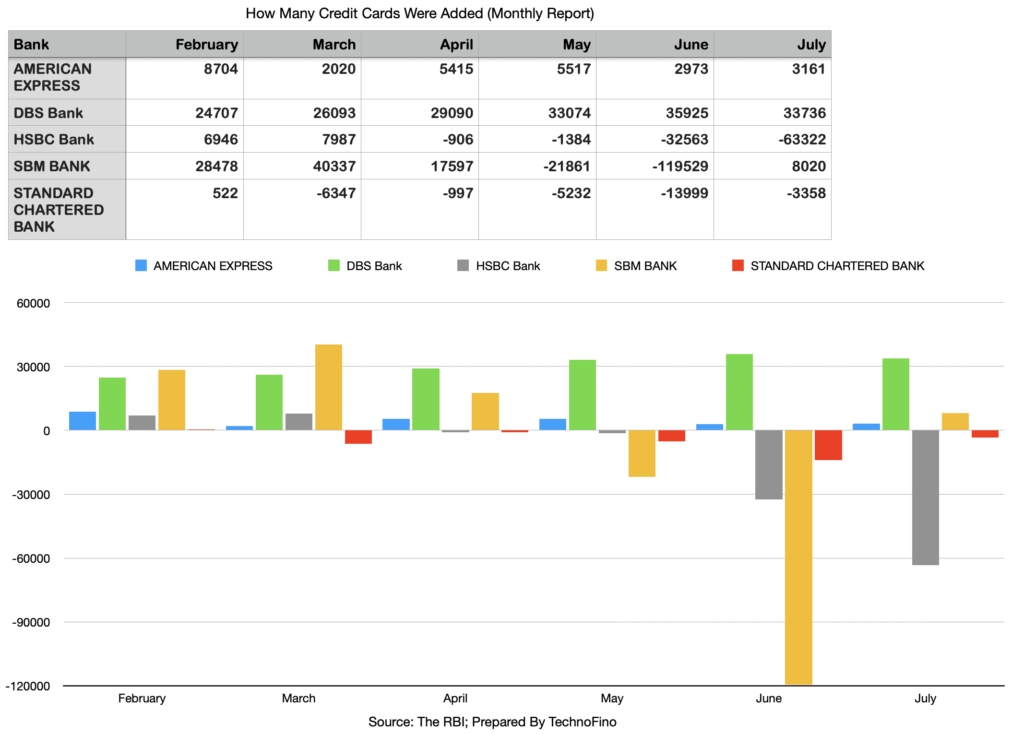

If you look at the above data sheet, you’ll find that Amex India is only adding approximately 4600 credit cards per month. HSBC Bank is in the negative, continuously losing customers after March 2023, and the numbers are high, which is a bit concerning for HSBC Bank. The same goes for Standard Chartered Bank; after February 2023, they are constantly losing customers. SBM Bank, known as a fintech-friendly bank, was growing rapidly last year, but due to some KYC and LRS transaction-related problems, they lost almost 1.4 lakhs credit cards. However, they have started to recover. They just need to fix their issues, and they can get back on track as they are associated with many growing fintech companies. SBM understands today’s generation and the importance of tech-friendly facilities.

On the other hand, DBS Bank is continuously growing. They have added almost 1,82,000 credit cards in the last 6 months, and the numbers are increasing. It might seem strange that without a strong credit card offering, DBS is managing to outperform other foreign banks with a very strong credit card portfolio like Amex, SC, and HSBC. Let me remind you that DBS Bank is issuing credit cards in partnership with Bajaj Finance. It’s because of Bajaj Fin that they are able to issue such a number of credit cards.

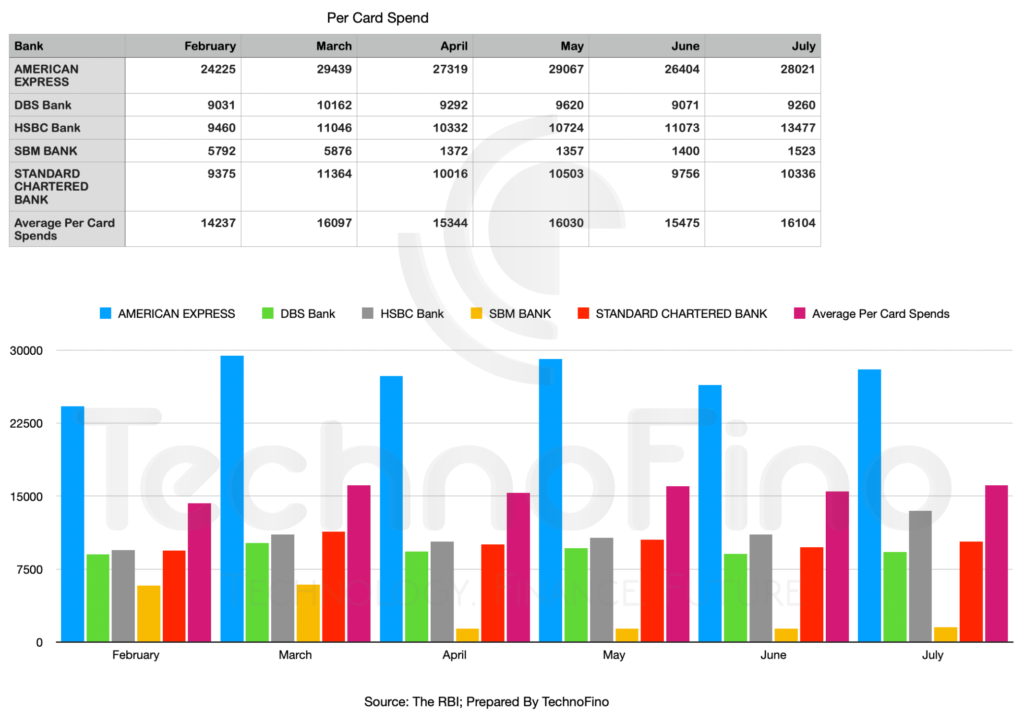

If you look at the per-card spending data, you can see that only Amex India is surpassing the average per-card spending figure by a significant margin. Standard Chartered, HSBC, and DBS Bank have per-card spends almost Rs. 5000 less than the industry average, while SBM Bank has the lowest figures, with cardholders spending only about Rs. 1400 per card. From this data, you can understand the importance of quality customers. At the end of the day, the business you receive from your customers is crucial, and Amex India is consistently doing an amazing job of maintaining such high per-card spending figures. In July, Amex had the highest per-card spending in India, and in June, they were in the second position.

But why are most foreign banks struggling in India? There are a few possible reasons:

- Limited Service Area: If you check the service areas of all struggling foreign banks, you’ll find that they serve a very limited number of cities, mostly metro cities. Big banks like HSBC, Standard Chartered, and Amex India only serve 10 to 13 cities in India. Recently, Amex India started offering their cards in Tier II cities as well. On the other hand, well-performing banks like SBM and DBS offer their credit cards in maximum Tier II and even Tier III cities.

- Less Banking Network: Foreign banks only have a physical presence in Tier I cities, so reaching more customers is a real challenge for them.

- Cross-Selling Credit Cards: As I already mentioned, foreign banks are only present in Tier I cities, so their customer base is also smaller compared to our Indian banks. More banking customers mean that the bank can cross-sell credit cards to more customers. But foreign banks lag behind in this aspect.

- Credit Card Benefits & Rewards: Good-quality products can be sold without much marketing. Most foreign banks have been offering the same credit cards for the last 5 years without any major changes or upgrades. However, in the last 2 or 3 years, Indian banks like HDFC Bank, SBI Card, Axis Bank, etc., have significantly upgraded their credit card offerings, launching multiple credit cards with amazing benefits and reward systems. Naturally, they are selling more credit cards than any foreign banks. Foreign banks should review their credit card portfolios and try to offer similar or better deals.

- High and Strict Eligibility Criteria: Most foreign banks have very high and strict eligibility criteria for their credit cards. Having a good credit score and income may not get you a credit card from banks like Standard Chartered or HSBC Bank. They analyze your credit profile, match your income with other credit card’s limit or loans you already have from the same or different banks, and then decide.

Those days are gone when people used to think that only those living in Tier I cities could have credit cards. There was a general assumption that only the elite class used credit cards, but this is far from true. You might think that merchants in Tier III cities or semi-rural areas wouldn’t have POS machines to accept credit cards, but surprisingly, many merchants in those areas do accept card payments. Moreover, nowadays, we can pay any small merchant using a RuPay credit card via the UPI network. This is the era of digital transactions; we shop online, order food online, buy electronics online, pay education fees online, pay taxes online, buy insurance online – everything is online. So, even people living in remote places are using credit cards for their online shopping and other payments.

Foreign banks need to break free from their old mindset. They must expand their service areas if they genuinely want to grow their business in India. They also need to simplify their application process. SBI Card, India’s second-largest credit card issuer, may overtake the largest card issuer, HDFC Bank, in a few months, all because of their reach. They are issuing credit cards in many rural areas, and the State Bank of India is present almost everywhere, boasting the largest banking network in India.

Selling credit cards solely in the name of exclusivity won’t work for long either. Amex India has always tried to follow this approach, selling cards in the name of exclusivity. However, over time, people have come to understand credit cards better. They are choosing lucrative benefits and rewards at lower prices over exclusivity.

Overall, this is a positive trend for Indian banks. Indian banks have been doing exceptionally well with their credit card offerings in recent times. But competition makes products better for consumers. Hopefully, we’ll see some fresh and lucrative offerings from a few foreign banks, at least from Amex India.

Meet Sumanta Mandal, the founder of Technofino, a renowned platform dedicated to providing valuable insights on credit cards and other banking products. With a profound knowledge of credit cards, Sumanta specializes in analyzing credit card reward systems and airmiles. His passion for the credit card industry drives him to delve deep into the intricacies of various credit card programs and uncover the best strategies to maximize rewards.

{kind=link}

You did not mention the biggest reason which is UPI and Rupay. Earlier UPI was mostly limited to small transaction and that too from bank account so it had no benefit of a credit limit. Now with UPI and Rupay coming together, most merchants hardly have any reason to allow any other network than Rupay and pay the network fee.