Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

-

Hey there! Welcome to TFC! View fewer ads on the website just by signing up on TF Community.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Has anyone got ₹100 per day Compensation for delayed update in credit bureaus i.e in credit reports as per RBI guidelines. Is it implemented or not?

- Thread starter cardy

- Start date

- Replies 26

- Views 3K

For these tagIs the RBI guideline implemented or not.

Has anyone got any amount as compensation at the rate ₹100 per day?

Have any idea?

@SSV @Vasuki @D₹V @Abhishek012 @Strange and more

@Tejo & @VISHESH_BANSAL legends

Yah the bamboo experts!

How did I forget? 😂

no compensation for delay in Normal updates as of now like account closed or present utilisation not updated, overdue update --- if 1,2,3 yrs then you will get ...Is the RBI guideline implemented or not.

Has anyone got any amount as compensation at the rate ₹100 per day?

Have any idea?

@SSV @Vasuki @D₹V @Abhishek012 @Strange and more

denifitely for wrong updates -- like wrong overdue updation,

So the framework has been implemented?no compensation for delay in Normal updates as of now like account closed or present utilisation not updated, overdue update --- if 1,2,3 yrs then you will get ...

denifitely for wrong updates -- like wrong overdue updation,

Right?

Can you send rbi guideline page url or pdf ??Has anyone got ₹100 per day Compensation for delayed update in credit bureaus i.e in credit reports as per RBI guidelines

There will conditions and exceptions in that guideline only

First tell what's your concern regarding update ?

Last edited:

Mostly there are only updation issues, it might be private or govt. exceptions for credit card default usersI think there supposed to be a nodal officer in the lending institutions has any bank provided any information regarding this?

Now due to fintechs and nbfcs ... overdue updations issues.

..... there will be nodal officer at all financial institutions but not specially for credit bureau updations, might Executives exist to solve issues.

Can you send rbi guideline page url or pdf ??

There will conditions and exceptions in that guideline only

First tell what's your concern regarding update ?

And

I have closed a vehicle loan in August 2021. All payments were debited from account by standing instruction. 100% on time payment.First tell what's your concern regarding update ?

But pnb updated 19rs overdue and delay payment for Jun and July as 93day and 123 days late.

After hundreds of complaints, emails, cibil rectification request overdue was corrected.

After RBI ombudsman complaint they admitted that they will correct it in 15days. It was sent to me in closure intimation.

Then they updated the dpds from 123 days to 1 and 93 days to 0

So in aug 23 it's still showing 1day, dpd and 1 delay payment in my credit score.

I have sent multiple emails and they just say we have forwarded the case to concerned department. But doesn't correct it.

I am thinking of another RBI ombudsman complaint citing previous ombudsman complaint's closure intimation that pnb is not abiding by RBI ombudsman and failed to update it inspite of promising to update in 15days. It's been 1 year since then.

You are eligible for compensation 😅I have closed a vehicle loan in August 2021. All payments were debited from account by standing instruction. 100% on time payment.

But pnb updated 19rs overdue and delay payment for Jun and July as 93day and 123 days late.

After hundreds of complaints, emails, cibil rectification request overdue was corrected.

After RBI ombudsman complaint they admitted that they will correct it in 15days. It was sent to me in closure intimation.

Then they updated the dpds from 123 days to 1 and 93 days to 0

So in aug 23 it's still showing 1day, dpd and 1 delay payment in my credit score.

I have sent multiple emails and they just say we have forwarded the case to concerned department. But doesn't correct it.

I am thinking of another RBI ombudsman complaint citing previous ombudsman complaint's closure intimation that pnb is not abiding by RBI ombudsman and failed to update it inspite of promising to update in 15days. It's been 1 year since then.

But 100/day from pnb .... 😵💫

But 10k is assured.

In compensation mention 10k and in description mention same clause and ask 100 per day for negligence and wanted doings...

pradeepG

TF Premier

do it ASAP, as it seems it is getting late...I have closed a vehicle loan in August 2021. All payments were debited from account by standing instruction. 100% on time payment.

But pnb updated 19rs overdue and delay payment for Jun and July as 93day and 123 days late.

After hundreds of complaints, emails, cibil rectification request overdue was corrected.

After RBI ombudsman complaint they admitted that they will correct it in 15days. It was sent to me in closure intimation.

Then they updated the dpds from 123 days to 1 and 93 days to 0

So in aug 23 it's still showing 1day, dpd and 1 delay payment in my credit score.

I have sent multiple emails and they just say we have forwarded the case to concerned department. But doesn't correct it.

I am thinking of another RBI ombudsman complaint citing previous ombudsman complaint's closure intimation that pnb is not abiding by RBI ombudsman and failed to update it inspite of promising to update in 15days. It's been 1 year since then.

Ok I'll make this happen in this weekdo it ASAP, as it seems it is getting late...

ARCHISMAN_DAS

TF Premier

My dad have a personal loan with a cooperative bank and from jan of this year the loan showing some overdue amount closely equal to the emi every month its getting updated same way since then and I visited the branch regarding this two times as they don't ve any sensible email support but they said there is no such due and that's pretty obvious because theres a SI for that loan so it's on auto pay but they denied to correct the cibil ...they said it's not their job.. on top of that the loan will be closed this July...how should I proceed now? Can I complaint on RBI regarding this?

You are eligible for compensation 😅

But 100/day from pnb .... 😵💫

But 10k is assured.

In compensation mention 10k and in description mention same clause and ask 100 per day for negligence and wanted doings...

A couple of months back, I got a compensation of ₹2000 from Axis bank as my UPI refund took 20 days. The transaction amount was ₹150. 😅Is the RBI guideline implemented or not.

Has anyone got any amount as compensation at the rate ₹100 per day?

Have any idea?

@SSV @Vasuki @D₹V @Abhishek012 @Strange and more

Karan.

TF Legend

This case is in-essence similar to yours, this might help you tooI have closed a vehicle loan in August 2021. All payments were debited from account by standing instruction. 100% on time payment.

But pnb updated 19rs overdue and delay payment for Jun and July as 93day and 123 days late.

After hundreds of complaints, emails, cibil rectification request overdue was corrected.

After RBI ombudsman complaint they admitted that they will correct it in 15days. It was sent to me in closure intimation.

Then they updated the dpds from 123 days to 1 and 93 days to 0

So in aug 23 it's still showing 1day, dpd and 1 delay payment in my credit score.

I have sent multiple emails and they just say we have forwarded the case to concerned department. But doesn't correct it.

I am thinking of another RBI ombudsman complaint citing previous ombudsman complaint's closure intimation that pnb is not abiding by RBI ombudsman and failed to update it inspite of promising to update in 15days. It's been 1 year since then.

Your case is a clear violation of RBI Ombudsman's advisory to IDFC/CRIF, if your latest CRIF report shows the false late payment.

- File a new complaint with RBI Ombudsman.

- In the new complaint, mention the old complaint number and the response that "IDFC removed the false late payment".

- Attach the latest CRIF report that shows the false late payment, to the new complaint.

- Humbly explain to RBI Ombudsman that IDFC misled RBI Ombudsman by responding that they (IDFC) removed the false late payment from CRIF.

- Request RBI to direct IDFC to remove the false late payment from CRIF.

- Mention that it has caused mental anguish, and negatively affected your CRIF score, thereby declined loan/credit card opportunities.

- Ask for 1Lakh as compensation i.e. the maximum allowed limit of compensation set by RBI Ombudsman. Mention 100000 in the compensation field.

- Keep checking your email's spam for any email from RBI Ombudsman. They may reach out to you wrt any clarification or response to other party's statement/denial. Usually RBI Ombudsman gives only 2-3 days to respond from the date of the email.

Also, suppose that IDFC had actually sent the removal request to CRIF but it was CRIF who did not execute that request, then write your complaint in a way that whosoever is at fault, they need to compensate you.

Yes you can but remember you will have to make a complain to the bank first. Only after 30 days over from that you can complain to rbio.My dad have a personal loan with a cooperative bank and from jan of this year the loan showing some overdue amount closely equal to the emi every month its getting updated same way since then and I visited the branch regarding this two times as they don't ve any sensible email support but they said there is no such due and that's pretty obvious because theres a SI for that loan so it's on auto pay but they denied to correct the cibil ...they said it's not their job.. on top of that the loan will be closed this July...how should I proceed now? Can I complaint on RBI regarding this?

So if email support is non-existent write a complain in a plain paper and handover to branch and take receipt. If denies then send it over registered post with acknowledgement. Send a copy of the same to the nodal officer or whatever authority is mentioned in their website. If they doesn't reply or reply unsatisfactorily make RBIO complaint.

ARCHISMAN_DAS

TF Premier

Thanks...they have a email mentioned on there website but they don't reply on that...Yes you can but remember you will have to make a complain to the bank first. Only after 30 days over from that you can complain to rbio.

So if email support is non-existent write a complain in a plain paper and handover to branch and take receipt. If denies then send it over registered post with acknowledgement. Send a copy of the same to the nodal officer or whatever authority is mentioned in their website. If they doesn't reply or reply unsatisfactorily make RBIO complaint.

TrueColours

TF Premier

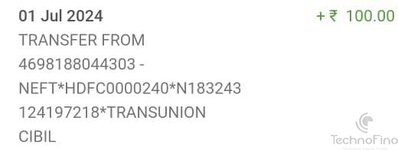

Framework for compensation to customers for delayed updation/ rectification of credit information - CIBIL paid compensation

The RBI vide its circular (RBI/2023-24/72) dated October 26, 2023, has directed CICs and CIs to implement a compensation framework for delayed updation/rectification of credit information. As per the said circular CIs have been granted a period of 21 calendar days and CICs have 9 calendar days to resolve a dispute (i.e. 30 days in total).

Failure of either the banks/financial Institutions and / or CICs entitles complainant to receive a compensation of ₹100/- for each day of delay from the banks/financial Institutions and/ or CIC (as applicable), shall be credited to the provided account details. This compensation framework becomes effective from April 26, 2024.

The compensation amount shall be credited to the bank account of the complainant within five (5) working days of the resolution of the complaint.

The complainant can approach RBI Ombudsman, under the Reserve Bank - Integrated Ombudsman Scheme, 2021, in case of wrongful denial of compensation by CIs or CICs.

This compensation framework becomes effective from April 26, 2024. Disputes initiated prior to April 26, 2024 and subsequently closed will not fall under the provisions of this circular, and therefore, compensation will not be applicable.

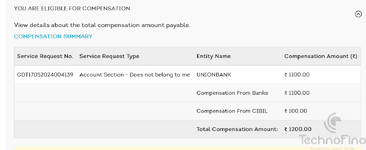

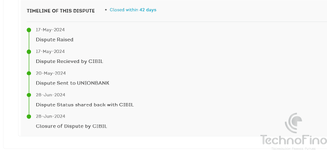

My case: Against Union Bank Of India - Reported wrong overdraft account to CIBIL

Complaint registered with a CIC (CIBIL) on May 17, 2024.

The CIC sought confirmation from the CI (in my case Union bank of India) on May 20, 2024. i. e. the CIBIL has taken 3 days to seek confirmation.

UBI provided confirmation to the CIBIL on June 28, 2024 (21st day would be June 07, 2024) – 21 days delay by UBI.

CIBIL closed my dispute on June 28, 2024. ( Bank rejected my complaint)

My complaint closed within 42days.

Maximum period granted to resolve a complaint: 30 days (in my case by June 16, 2024)

Delay = 42 – 30 = 12 days.

Compensation per day = ₹100

Total Compensation amount = 12 × 100 = ₹1200

CIBIL paid Rs.100 compensation and waiting for Rs.1100 compensation from UBI.

The RBI vide its circular (RBI/2023-24/72) dated October 26, 2023, has directed CICs and CIs to implement a compensation framework for delayed updation/rectification of credit information. As per the said circular CIs have been granted a period of 21 calendar days and CICs have 9 calendar days to resolve a dispute (i.e. 30 days in total).

Failure of either the banks/financial Institutions and / or CICs entitles complainant to receive a compensation of ₹100/- for each day of delay from the banks/financial Institutions and/ or CIC (as applicable), shall be credited to the provided account details. This compensation framework becomes effective from April 26, 2024.

The compensation amount shall be credited to the bank account of the complainant within five (5) working days of the resolution of the complaint.

The complainant can approach RBI Ombudsman, under the Reserve Bank - Integrated Ombudsman Scheme, 2021, in case of wrongful denial of compensation by CIs or CICs.

This compensation framework becomes effective from April 26, 2024. Disputes initiated prior to April 26, 2024 and subsequently closed will not fall under the provisions of this circular, and therefore, compensation will not be applicable.

My case: Against Union Bank Of India - Reported wrong overdraft account to CIBIL

Complaint registered with a CIC (CIBIL) on May 17, 2024.

The CIC sought confirmation from the CI (in my case Union bank of India) on May 20, 2024. i. e. the CIBIL has taken 3 days to seek confirmation.

UBI provided confirmation to the CIBIL on June 28, 2024 (21st day would be June 07, 2024) – 21 days delay by UBI.

CIBIL closed my dispute on June 28, 2024. ( Bank rejected my complaint)

My complaint closed within 42days.

Maximum period granted to resolve a complaint: 30 days (in my case by June 16, 2024)

Delay = 42 – 30 = 12 days.

Compensation per day = ₹100

Total Compensation amount = 12 × 100 = ₹1200

CIBIL paid Rs.100 compensation and waiting for Rs.1100 compensation from UBI.

Attachments

real_name_hidden

TF Premier

I got compensation from standard chartered citing above rbi circular for removal of double enquiry not done within 30 days of complain to bank.

Similar threads

- Question

- Replies

- 3

- Views

- 465

- Replies

- 5

- Views

- 1K

- Replies

- 13

- Views

- 2K