The

main advantage will be on Travel edge and for spends on more than 1.5L a month. So, if we spend 2.5L in a month, 1.5L will earn 12ER, and 1L will earn 35ER. 1L @ 35 ER will fetch us around 17k ER.I have the DCB LTF as I had the moneyback for a few years and for a whole year I had spends of 5 lakhs/month and no defaults in payments of the same amount. I was offered DCB LTF when HDFC bank was banned from issuing new customers by RBI and they gave great upgrades to existing customers.

I do not travel a lot. (Though I would love to). 2013-2017 I had no international travel and 2018 I went to Canada, South Africa nad Maldives and 2019 I could go to Armenia in a friend's wedding. Again with COVID 2020 and 2021 no international travel. Last year I went to South Korea in August and finished the year with a trip to Dubai in December.

I love unlimited lounge access on DCB. (I have taken domestic flights more often though) and I just got the Axis Magnus in July so I am not sure if I will keep it after a year if the devaluation is this bad and I have to pay 12500 + GST and get nothing for that and nothing for 1 lakh spends per month.

My spends are not too much and DCB being LTF (and thus all HDFC cards LTF as a consequence - HDFC tata Neu and UPI Virtual as well because I have not been charged the 250 joining fees yet), I guess I will discontinue Magnus at the end of the 1st year. I hope my limit remains high though. I got it same as DCB at 828k and Axis sucks at LE. before this even after 10 years of holding Axis cards my limit is just 180k which was shared on Axis Ace, Axis FK and Kiwi. I had 4 cards after Magnus was approved but I did cancel Fk after the devaluation, so I am back to 3 now.

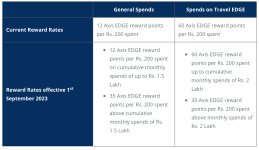

Attachments