Hi Friends,

Below are the new income tax slab and applicable rate for FY 2025-26, as per the budget announcement by our Finance Minister dated Feb. 1, 2025.

I have also calculated taxpayers' net savings (based on reference income) for your quick reference based on the recent tax cut announcement after a long time.

Income Tax Slab & Rate (New Tax Regime): FY 2025-26 (Applicable for filling ITR in July/Sept., 2026)

For Individuals (Resident or Non-Resident) less than 60 years of age at any time during the previous year:

*Surcharge (10-25%) applicable on income above 50 Lakh.

*The Rate of Health & Education Cess 4% (additional).

**Calculation excludes any other exemptions and deductions applicable on a case-to-case basis. Exemptions and deductions should be calculated first to determine your taxable income. For example, salaried individuals get ₹ 75,000 additional standard deduction.

**Tax Rebate applicable for income up to ₹ 12 Lakh. Tax rebates are not applicable on special income (e.g., capital gains).

Marginal benefits available from ₹ 12,00,000 to ₹ 12,70,600. In simple terms, at ₹ 12L, you pay zero tax, but at ₹ 12,70,600, you need to pay ₹ 70,600 as tax. Afterwards, taxes are charged at the applicable slab rate. (Please keep in mind that effectively, for salaried taxpayers, tax rebates are applicable up to ₹ 12,75,000, and marginal benefits are available up to ₹ 13,45,600).

You will get the maximum benefit if your income is up to 12 Lakh. However, the maximum absolute gain will be around 24 Lakh.

*** The First bracket indicates Savings in leu of Health and Education Cess. The third bracket indicates Tax Savings in percentage.

(Tax Milestones) Income vs effective tax amount and rate:

@ ₹ 12.0 Lakh, tax liability is zero (0.0%).

@ ₹ 15.67 Lakh, tax liability becomes ₹ 1 Lakh (6.4%).

@ ₹ 20 Lakh, tax liability becomes ₹ 2 Lakh (10.0%)

@ ₹ 24 Lakh, tax liability becomes ₹ 3 Lakh (12.5%).

@ ₹ 27.33 Lakh, tax liability because ₹ 4 Lakh (14.6%).

@ ₹ 30.67 Lakh, tax liability becomes ₹ 5 Lakh (16.3%).

For about 95% of taxpayers, the new tax regime should be beneficial.

On average, if your additional deduction amount (Old vs. New regime) is more than ₹ 8 Lakh, then only the old tax regime would be beneficial.

----------------------------------------------------------------------

Income Tax Slab & Rate (New Vs Old Regime): FY 2024-25 (Applicable for filling ITR in July/Sept., 2025)

For Individuals (Resident or Non-Resident) less than 60 years of age at any time during the previous year:

Surcharge (10-25%) applicable on income above 50 Lakh.

The Rate of Health & Education Cess 4% (additional).

--------

For more information, please visit:

Ref (1): https://www.incometax.gov.in/iec/foportal/help/individual/return-applicable-1

Ref (2): https://www.incometax.gov.in/iec/foportal/help/individual-business-profession

Ref (3): https://www.bajajfinserv.in/investments/income-tax-slabs

Below are the new income tax slab and applicable rate for FY 2025-26, as per the budget announcement by our Finance Minister dated Feb. 1, 2025.

I have also calculated taxpayers' net savings (based on reference income) for your quick reference based on the recent tax cut announcement after a long time.

Income Tax Slab & Rate (New Tax Regime): FY 2025-26 (Applicable for filling ITR in July/Sept., 2026)

For Individuals (Resident or Non-Resident) less than 60 years of age at any time during the previous year:

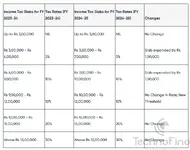

New Tax Slab (FY 2025-26) | Revised Tax Rate * (Feb 1, 2025 Budget) | **Actual Income (for reference) | Net Tax Savings *** |

| Up to ₹ 4 Lakh | Nil | ₹ 8 Lakh | ₹ 30,000 (+1200) [100%] |

| ₹ 4 - ₹ 8 Lakh | 5% above ₹ 4 Lakh | ₹ 10 Lakh | ₹ 50,000 (+2000) [100%] |

| ₹ 8 - ₹ 12 Lakh | ₹ 20,000 + 10% above ₹ 8 Lakh | ₹ 12 Lakh | ₹ 80,000 (+3200) [100%] |

| ₹ 12 - ₹ 16 Lakh | ₹ 60,000 + 15% above ₹ 12 Lakh | ₹ 14 Lakh | ₹ 30,000 (+1200) [25.0%] |

| ₹ 16 - ₹ 20 Lakh | ₹ 120,000 + 20% above ₹ 16 Lakh | ₹ 16 Lakh | ₹ 50,000 (+2000) [29.4%] |

| ₹ 20 - ₹ 24 Lakh | ₹ 2,00,000 + 25% above ₹ 20 Lakh | ₹ 18 Lakh | ₹ 70,000 (+2800) [30.4%] |

| Above ₹ 24 Lakh | ₹ 3,00,000 + 30% above ₹ 24 Lakh | ₹ 20 Lakh | ₹ 90,000 (+3600) [31.0%] |

| ₹ 22 Lakh | ₹ 1.0 Lakh (+4000) [28.6%] | ||

| ₹ 24 Lakh and Above | ₹ 1.1 Lakh (+4400) [up to 26.8%] |

*Surcharge (10-25%) applicable on income above 50 Lakh.

*The Rate of Health & Education Cess 4% (additional).

**Calculation excludes any other exemptions and deductions applicable on a case-to-case basis. Exemptions and deductions should be calculated first to determine your taxable income. For example, salaried individuals get ₹ 75,000 additional standard deduction.

**Tax Rebate applicable for income up to ₹ 12 Lakh. Tax rebates are not applicable on special income (e.g., capital gains).

Marginal benefits available from ₹ 12,00,000 to ₹ 12,70,600. In simple terms, at ₹ 12L, you pay zero tax, but at ₹ 12,70,600, you need to pay ₹ 70,600 as tax. Afterwards, taxes are charged at the applicable slab rate. (Please keep in mind that effectively, for salaried taxpayers, tax rebates are applicable up to ₹ 12,75,000, and marginal benefits are available up to ₹ 13,45,600).

You will get the maximum benefit if your income is up to 12 Lakh. However, the maximum absolute gain will be around 24 Lakh.

*** The First bracket indicates Savings in leu of Health and Education Cess. The third bracket indicates Tax Savings in percentage.

(Tax Milestones) Income vs effective tax amount and rate:

@ ₹ 12.0 Lakh, tax liability is zero (0.0%).

@ ₹ 15.67 Lakh, tax liability becomes ₹ 1 Lakh (6.4%).

@ ₹ 20 Lakh, tax liability becomes ₹ 2 Lakh (10.0%)

@ ₹ 24 Lakh, tax liability becomes ₹ 3 Lakh (12.5%).

@ ₹ 27.33 Lakh, tax liability because ₹ 4 Lakh (14.6%).

@ ₹ 30.67 Lakh, tax liability becomes ₹ 5 Lakh (16.3%).

For about 95% of taxpayers, the new tax regime should be beneficial.

On average, if your additional deduction amount (Old vs. New regime) is more than ₹ 8 Lakh, then only the old tax regime would be beneficial.

----------------------------------------------------------------------

Income Tax Slab & Rate (New Vs Old Regime): FY 2024-25 (Applicable for filling ITR in July/Sept., 2025)

For Individuals (Resident or Non-Resident) less than 60 years of age at any time during the previous year:

| Old Tax Regime | New Tax Regime u/s 115BAC | ||

| Income Tax Slab | Income Tax Rate | Income Tax Slab | Income Tax Rate |

| Up to ₹ 2,50,000 | Nil | Up to ₹ 3,00,000 | Nil |

| ₹ 2,50,001 - ₹ 5,00,000 | 5% above ₹ 2,50,000 | ₹ 3,00,001 - ₹ 7,00,000 | 5% above ₹ 3,00,000 |

| ₹ 5,00,001 - ₹ 10,00,000 | ₹ 12,500 + 20% above ₹ 5,00,000 | ₹ 7,00,001 - ₹ 10,00,000 | ₹ 20,000 + 10% above ₹ 7,00,000 |

| Above ₹ 10,00,000 | ₹ 1,12,500 + 30% above ₹ 10,00,000 | ₹ 10,00,001 - ₹ 12,00,000 | ₹ 50,000 + 15% above ₹ 10,00,000 |

| ₹ 12,00,001 - ₹ 15,00,000 | ₹ 80,000 + 20% above ₹ 12,00,000 | ||

| Above ₹ 15,00,000 | ₹ 1,40,000 + 30% above ₹ 15,00,000 |

The Rate of Health & Education Cess 4% (additional).

--------

For more information, please visit:

Ref (1): https://www.incometax.gov.in/iec/foportal/help/individual/return-applicable-1

Ref (2): https://www.incometax.gov.in/iec/foportal/help/individual-business-profession

Ref (3): https://www.bajajfinserv.in/investments/income-tax-slabs

Last edited: