My AXIS Relationship Manager (RM) is offering me a ULIP (Unit Linked Insurance Plan).

I’m usually against ULIPs because of the well-known drawbacks, but this one seems worth considering for me atleast.

Given these factors, is this a good option, or are there better alternatives?

PS: I used ChatGPT to optimize the post.

I’m usually against ULIPs because of the well-known drawbacks, but this one seems worth considering for me atleast.

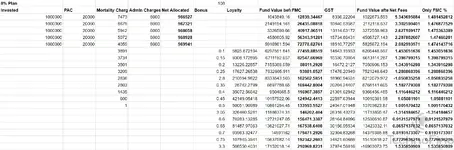

- Investment Details:

- It’s a ₹10 lakh plan, out of which ₹9.66 to ₹9.7 lakh is invested.

- The Fund Management Charge (FMC) is on par with direct mutual funds.

- It has a lock-in period of 5 years.

- Term Plan Concerns:

- I need a term insurance plan, but I’m hesitant because of:

- The hassle of medical checkups.

- Potential stress for my family during claim settlement.

- Higher premiums due to my weight.

- On PolicyBazaar, many companies are refusing me a term plan because I haven’t completed my 12th grade.

- I need a term insurance plan, but I’m hesitant because of:

- Cost Analysis:

- For a standalone term plan, I’d be paying around ₹20k per year (₹14k base + additional costs for being overweight + GST).

- The FMC is falling around 0.5-1.5% over 20 years, with the last 10 years being under 1% on average. Which is on par with Direct Mutual Funds.

Given these factors, is this a good option, or are there better alternatives?

PS: I used ChatGPT to optimize the post.

Attachments