I’ve made it clear I don’t want term insurance. This decision is based on past issues with such providers and my family’s inability to handle potential disputes. I won’t risk even a 1% chance of them losing the payout when I can guarantee it for ₹10k–₹15k more per year.There are many insurers, including Max Life itself, that issue term plans to those having min 10th pass qualifications. You can buy term plan, just that you do not want to. That is a decision from your side.

Wouldn't the term plan lapse if I do survive post-20?Combination of term plan+MF would give significantly higher death benefits than this option right till 20th year and min 20-25% higher survival benefits in case the insured remains alive after 20 years.

That’s exactly why I’m leaning toward this one—their performance has been impressive, with the NAV climbing from 30 to 120 in the past five years.For ULIP performance, never compare with regular MF. Comparison can only be made with similar ULIPs. Almost all AMCs use least aggressive investment pattern for ULIPs. So growth in investment portion of ULIP is significantly lower than normal MF.

I’m comparing it to mutual funds because the combination of a term plan + MF would need to deliver similar returns to make sense. That’s why I’m evaluating this ULIP against MF performance rather than other ULIPs.

The fees they are charging are on Par with MF as well.

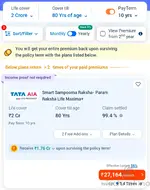

The plan they are referring me to is this - https://www.moneycontrol.com/insura...-capital-builder-high-growth-fund-IMA061.html

If I pick their last 10yrs annualized return is 19.71%.

That gives me IRR of 20.51% AFTER all fees and shit getting deducted.

This is the closest IRL calculation I get to for this fund.

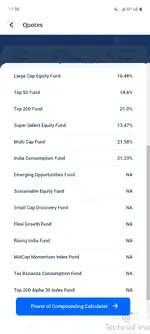

ULIPs are bad because of all the charges they put especially due to riders and all, but here the charges are actually quite minimal.

The only outrageous charge that I feel is there, are the PAC & Admin Charges of 26k++ for first 5yrs (aka paying term).