suneelkumar206@

TF Select

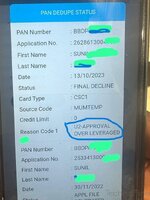

Currently I hold close to 10 cards with ITR of 30L & overall credit limit across all the cards 43L.

I don't have any SBI credit card and looking to apply one.

CIBIL of 781 & no defaults.

So my question is am I over leverage according to SBI??

Shall I apply directly or reduce my exposure?

I don't have any SBI credit card and looking to apply one.

CIBIL of 781 & no defaults.

So my question is am I over leverage according to SBI??

Shall I apply directly or reduce my exposure?