Initially I did not care much about this non reporting of credit limit issue despite having an HDFC CC, since my CIBIL Score is perfectly fine even with an HDFC card. But seeing a lot of confusion on this thread, I decided to dig some details myself. Initially, I searched about this issue from Indian sources, but was not able to find any significant info on this. Then I thought of looking into foreign sources of information. Since HDFC does not issue its credit cards outside India(Maybe, but it would be very low in number), I decided to look for a card with similar credit reporting like HDFC Bank. And the cards which struck me instantly were the Amex Charge cards. I don't have an Amex charge card, but came to know from the Internet that it also does not report its credit limit to the rating agencies. On searching the internet for some time, I came across these videos and articles;

On the surface, charge cards and credit cards look almost the same. Both payment methods are around 3.37 by 2.125 inches and generally made of plastic or, in some cases, metal. You use charge cards and credit cards to pay for purchases and repay the card issuer at a later date. And either type may a

www.forbes.com

Many of Amex's best rewards cards are charge cards rather than credit cards. Learn about the implications for your credit score and credit utilization ratio.

thepointsguy.com

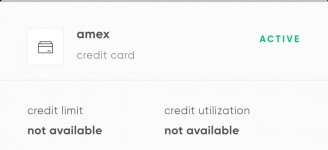

I do not know about the much about the YouTube channel of the video I shared, but the other 2 articles are from reputed sources. The last article by 'The Points Guy' in fact, showed a TransUnion (parent of CIBIL, India)credit report screenshot of an Amex Charge card. In the screenshot, it was shown that no credit limit was reported for the charge card and the credit utilisation ratio was 'N/A'. All the 3 sources I have claimed the same thing that Credit Utilisation Ratio is NOT considered in calculating your FICO score through your Charge Card account.

Now since TransUnion is the parent company of CIBIL and HDFC cards' reporting is quite similar to Charge Cards' reporting, I am pretty confident that Credit Card Utilisation Ratio is NOT considered in calculating your CIBIL score through your HDFC CC account. At least I have not seen anyone hurting his/her credit score solely because of an HDFC card.

Hope this clears all the doubts regarding this issue. Any corrections and suggestions are welcome.