Greetings everyone,

The Reserve Bank of India (RBI) issued new guidelines for credit card issuers on April 21st, 2022, which came into effect on July 1st, 2022. The RBI has explicitly stated in these guidelines that credit card issuing companies and banks must provide a written explanation for rejecting an applicant's card application. This information can be found in paragraph 6. (a) i. of "RBI/2022-23/92 DoR.AUT.REC.No.27/24.01.041/2022-23" dated April 21st, 2022.

I'm quoting the paragraph here "Card-issuers shall provide a one-page Key Fact Statement along with the credit card application containing the important aspects of the card such as rate of interest, quantum of charges, among others. In case of rejection of a credit card application, the card-issuer shall convey in writing the specific reason/s which led to the rejection of the application."

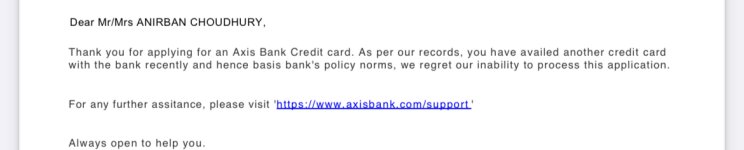

However, it has come to our attention that many banks are not following this rule. When a bank rejects a credit card or other credit product such as loan application, they often provide a vague reason such as "Internal Criteria" instead of specifying the exact reason for the rejection. When a customer files a complaint with the RBI banking ombudsman seeking further clarification, the ombudsman often closes the case under clause 16 without proper investigation.

We would like to question the Reserve Bank of India (RBI) on the rationale behind implementing the guideline requiring credit card issuers and banks to provide a written explanation for rejecting an applicant's card application. While this guideline is a step in the right direction, we believe that there is still room for improvement.

If we examine the credit card application process in many developed countries such as the USA, we can see that all credit card issuers provide an exact reason for rejecting an application. This practice is backed by a law that protects the interests of customers, known as the Equal Credit Opportunity Act. We believe that India should follow in the footsteps of these countries to ensure that customers are not left in the dark about the reasons for their credit card application rejection.

Despite being ahead of the USA in terms of digital transactions, our credit card application process lacks transparency. This lack of transparency can be frustrating for customers, who are left without a clear understanding of why their application was rejected. Therefore, we urge the RBI to take steps to enhance transparency in the credit card application process, such as implementing a law similar to the Equal Credit Opportunity Act. By doing so, we can ensure that customers have a fair and transparent experience when applying for a credit card in India.

We request the RBI to strictly enforce the existing guideline ("RBI/2022-23/92 DoR.AUT.REC.No.27/24.01.041/2022-23" dated April 21st, 2022, paragraph 6. (a) i.) and ensure that the ombudsman officer does not close a case under clause 16 if a customer escalates the issue with them.

If you agreed with us, sign petition on change - https://chng.it/9Y59tHYBDh

The Reserve Bank of India (RBI) issued new guidelines for credit card issuers on April 21st, 2022, which came into effect on July 1st, 2022. The RBI has explicitly stated in these guidelines that credit card issuing companies and banks must provide a written explanation for rejecting an applicant's card application. This information can be found in paragraph 6. (a) i. of "RBI/2022-23/92 DoR.AUT.REC.No.27/24.01.041/2022-23" dated April 21st, 2022.

I'm quoting the paragraph here "Card-issuers shall provide a one-page Key Fact Statement along with the credit card application containing the important aspects of the card such as rate of interest, quantum of charges, among others. In case of rejection of a credit card application, the card-issuer shall convey in writing the specific reason/s which led to the rejection of the application."

However, it has come to our attention that many banks are not following this rule. When a bank rejects a credit card or other credit product such as loan application, they often provide a vague reason such as "Internal Criteria" instead of specifying the exact reason for the rejection. When a customer files a complaint with the RBI banking ombudsman seeking further clarification, the ombudsman often closes the case under clause 16 without proper investigation.

We would like to question the Reserve Bank of India (RBI) on the rationale behind implementing the guideline requiring credit card issuers and banks to provide a written explanation for rejecting an applicant's card application. While this guideline is a step in the right direction, we believe that there is still room for improvement.

If we examine the credit card application process in many developed countries such as the USA, we can see that all credit card issuers provide an exact reason for rejecting an application. This practice is backed by a law that protects the interests of customers, known as the Equal Credit Opportunity Act. We believe that India should follow in the footsteps of these countries to ensure that customers are not left in the dark about the reasons for their credit card application rejection.

Despite being ahead of the USA in terms of digital transactions, our credit card application process lacks transparency. This lack of transparency can be frustrating for customers, who are left without a clear understanding of why their application was rejected. Therefore, we urge the RBI to take steps to enhance transparency in the credit card application process, such as implementing a law similar to the Equal Credit Opportunity Act. By doing so, we can ensure that customers have a fair and transparent experience when applying for a credit card in India.

We request the RBI to strictly enforce the existing guideline ("RBI/2022-23/92 DoR.AUT.REC.No.27/24.01.041/2022-23" dated April 21st, 2022, paragraph 6. (a) i.) and ensure that the ombudsman officer does not close a case under clause 16 if a customer escalates the issue with them.

If you agreed with us, sign petition on change - https://chng.it/9Y59tHYBDh