I made a mistake by borrowing money through the Slice app. My friend borrowed 25k under my name and didn't make the payments on time. How much days it would take to get atleast 700score☹️. Loan has been cleared now(a week ago)

If you already have an HDFC account, then an HDFC card might be better because there's a high chance that they'll offer you a non-FD credit card later.

Actually, you don't need to open a bank account to get FD cards. For example, you don't need an IDFC savings account to get the IDFC First Woow FD credit card.

Never borrow for someone else on your name. This is the biggest mistake you can do. When you take out a loan, irrespective of the circumstances, you have to repay the loan back.

Yes.

He misled me by saying that nothing would happen because the Slice app is against RBI rules. + We still being a student I didn't had any source of income to clear this.

One is biggest mistake of my life.

If you already have an HDFC account, then an HDFC card might be better because there's a high chance that they'll offer you a non-FD credit card later.

Actually, you don't need to open a bank account to get FD cards. For example, you don't need an IDFC savings account to get the IDFC First Woow FD credit card.

If you can afford there are two practical thing to do

1- Get 5-10k fd credit card ( u won't close it atleast in future.

For 2-10k take idfc wow card

Or 50k-100k icici plat chip card ( recommended ) both as per appetite

2- buy cibil subscription ( if u can afford totally optional )

With crystal 🔮 ball here are few things

1 - if closed the bad loan remark.

Cibil will be back to 700+

For 750 it would take 2-3 month..

What is your other cibil profile/ other loan added

Had defaulted my hdfc cc payment by 3 months 7 years ago.

Scored dropped to near your scores. I believe 500 or 600 don’t recollect properly.

I cleared the entire outstanding, in a month and the card account got closed. After I think a month or two scores went back up to near 700 or little above.

HDFC kept reporting payment even though account was closed. The next account I ever had was Paytm pay later I never bothered to apply for a cc thinking banks will outright reject me.

I started getting pre approved offers about a year after pay later but still did not take any. Now I have 4 cards.

The fastest way for you to improve is to take a secured credit card. Use and pay on time. You will start getting pre approved offers as scores go up.

Every one has a bad phase in life. Let me share my experience with CIBIL score. I was in a difficult phase and defaulted on couple of credit cards. Could not clear them for years. Below are the points to note

1. You have to clear your complete outstanding (do not got for settlement). If you choose settlement then the account in CIBIL will show as settled and not closed. It is very difficult to get unsecured loans or credit cards if your report shows settled

2. It will take couple of years at least for the score to increase

3. If you plant to take the FD based credit card, make share to take the highest FD. This will help keep your utilisation low. Make sure your utilisation is less than 30% on the FD card. Make the payment before the CIBIL report date to keep utilisation low

4. Do not default on any future payments

My score was 585 in 2017 now it’s at 790.

CIBIL score is just 1 factor banks consider to give loans but also an important one

Focus on increasing your income while the score increases

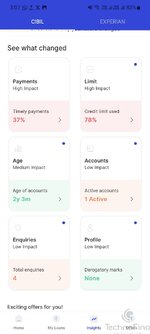

Get more than 1 Secured CC and as many as possible BNPL. But do not use any this will increase your on time payment count and current on time payment percentage will improve from 37% currently.