I am afraid that the opportunity cost is around 33%+. The following table is based on the policy that my father bought 💀

I have considered a 23% annualized return for any fund.

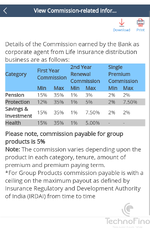

View attachment 63341

I am not fully confident about these calculations, have to put more effort. Too many charges, I think I have excluded GST. Let the questions come so that I will be motivated to refine it. Tired rn, will revisit it in a few days. ChatGPT is also not functioning properly.