Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

-

Hey there! Welcome to TFC! View fewer ads on the website just by signing up on TF Community.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

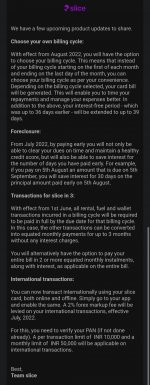

Upcoming changes in Slice card

- Thread starter prc1990

- Start date

- Replies 60

- Views 7K

Can you explain.But they showed very low amount of 5 k if he spends more than 5 i think it will be bad for his score

akshayhs

TF Legend

Not true. There are times where I used 100% of limit but promptly cleared the dues well ahead of time. I didn't see any variation in my scores during this period of high usage. My account was with QUADFIN was well.But they showed very low amount of 5 k if he spends more than 5 i think it will be bad for his score

akshayhs

TF Legend

Surprisingly, I checked my latest credit report and the new NBFC has marked the sanctioned limit back to 5k. It was initially reported in full. (60k)It's quite good as it shows as loan in cibil if they shown full limit it will be a trouble in future for getting unsecured credit card or loans

Quite interesting.Surprisingly, I checked my latest credit report and the new NBFC has marked the sanctioned limit back to 5k. It was initially reported in full. (60k)

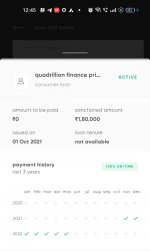

Just got a CRIF refresh and it shows the actual/entire limit i.e. 180K whereas CIBIL and EXPERIAN show as 5K only.QUADFIN now shows up in CIBIL as well with credit limit reported as 5K only which is good as well as bad if spends spill over to more than 5K.

Also CRIF shows payment history since Nov'21 and CIBIL & EXPERIAN show since Apr'22. Different data points altogether.

Attachments

I can now confirm they have started reporting the entire limit to CIBIL, EXPERIAN and CRIF. In fact in CIBIL, full limit has been reported under the header "High Credit" instead of the header "Credit Limit".Recently slice has been taking some precautions to not fully destroy cibil. According to CSR they are reporting just 10% of total sanctioned limit so the people with high limit don't add up the limit as unsecured loan.

So time to close the Slice permanently.

Wait for some months. They will eventually report the entire limit back. I noticed the same behaviour with CIBIL, EXPERIAN and CRIF in gap of few months and hence, harmful being classified as Consumer Loan.Surprisingly, I checked my latest credit report and the new NBFC has marked the sanctioned limit back to 5k. It was initially reported in full. (60k)

It's time to close the account.

I can confirm too that Slice is reporting full limit atleast in CIBIL

It's not good 😐...Wait for some months. They will eventually report the entire limit back. I noticed the same behaviour with CIBIL, EXPERIAN and CRIF in gap of few months and hence, harmful being classified as Consumer Loan.

It's time to close the account.

akshayhs

TF Legend

You're right. After the repayment tomorrow, I am opening a support ticket asking them to close my account permanently.Wait for some months. They will eventually report the entire limit back. I noticed the same behaviour with CIBIL, EXPERIAN and CRIF in gap of few months and hence, harmful being classified as Consumer Loan.

It's time to close the account.

Try your luck.. it was quite difficult with bnpl. I am running with LazyPay team from around 2 months still only cibil got closed rest are still open .. tried raising complaint with rbi still they are rock solid 😂 .You're right. After the repayment tomorrow, I am opening a support ticket asking them to close my account permanently.

It would be reported as closed to other 3 CICs eventually as it takes time. CIBIL is much faster. So hold on to your patience 🙅.Try your luck.. it was quite difficult with bnpl. I am running with LazyPay team from around 2 months still only cibil got closed rest are still open .. tried raising complaint with rbi still they are rock solid 😂 .

3 month with LazyPay still holding and it took around 8 months for paytm postpaid. Flipkart and mobikwik was around 45 days as they were backed by idfc bank . So i directly called them and ask them to close .It would be reported as closed to other 3 CICs eventually as it takes time. CIBIL is much faster. So hold on to your patience 🙅.

akshayhs

TF Legend

Even with RBI ombudsman involved?3 month with LazyPay still holding and it took around 8 months for paytm postpaid. Flipkart and mobikwik was around 45 days as they were backed by idfc bank . So i directly called them and ask them to close .

AsB

TF Legend

Get Credit Cards , especially RuPay Cards. Those who say that BNPLs are the new Credit Cards, well , now is not the time for their uprising. I had closed PayTM postpaid, but it was finally closed in CIBIL after 8-9 months, after continuous followups and RBI complaint. Similarly, Amazon Pay Later was not closed in CIBIL for around 5-6 months, again after continuous follow ups. These BNPL companies threaten your families and friends if you miss a payment.

Wait for RBI to come up with a master plan. Otherwise, take One Card, if you are not getting any other Credit Card.

Wait for RBI to come up with a master plan. Otherwise, take One Card, if you are not getting any other Credit Card.

Y

Yes they take them also for granted 😂. It seems jokes for them . Stay away from credit lines . They are toxic 😅 if you ever missed by 1 day .. your scores going to be ruined and your friends and family will be expecting calls from them .Even with RBI ombudsman involved?

True 🤣Y

Yes they take them also for granted 😂. It seems jokes for them . Stay away from credit lines . They are toxic 😅 if you ever missed by 1 day .. your scores going to be ruined and your friends and family will be expecting calls from them .

Manu624

TF Buzz

True.....I have total 17 loans from zest only

I can now confirm they have started reporting the entire limit to CIBIL, EXPERIAN and CRIF. In fact in CIBIL, full limit has been reported under the header "High Credit" instead of the header "Credit Limit".

So time to close the Slice permanently.

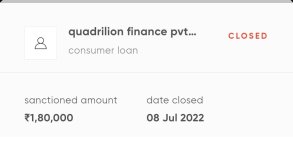

Slice has now been reported as closed in EXPERIAN.

Attachments

aryanmahajan2506

TF Buzz

It will show the total limit issued to you as a consumer loan in your cibil score. This goes for any BNPL service.I have one question regarding the slice and uni pay. Suppose last month i spend 20k and paid it Fully now next month i spend 30k paid it Fully how will slice or uni pay show in my cibil ? As consumer durable loan? For every month bill it will show loan? Like if i spend 10k in june and 10 ki in july so it will show 2 different loan? Or just on single?

Similar threads

- Replies

- 252

- Views

- 16K

- Replies

- 9

- Views

- 753

- Replies

- 1

- Views

- 355

- Replies

- 2

- Views

- 286