chuckzspadina

TF Select

Hey everyone! I wanted to share my recent experience with the AU LIT credit card, which has been nothing short of amazing. Last month, I managed to get a return of around 10% on my spending, and here’s how it all added up:

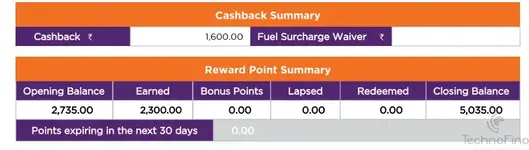

Cashback Highlights:

Total Cashback Received: ₹1,600.00

Reward Points Breakdown:

Points Earned: 2,300

Each reward point is worth ₹0.25, so the 2,300 points I earned last month are equivalent to ₹575.00.

Although I don’t have the SBI Cashback card, the AU LIT credit card has not disappointed me at all. It not only gave me substantial cashback but also helped me rack up a ton of reward points. These points can be redeemed for a variety of rewards, making every purchase feel even more worthwhile.

If you’re on the lookout for a credit card that offers great returns and rewards, I highly recommend giving the AU LIT credit card a try. It’s been a game-changer for me!

Cashback Highlights:

Total Cashback Received: ₹1,600.00

Reward Points Breakdown:

Points Earned: 2,300

Each reward point is worth ₹0.25, so the 2,300 points I earned last month are equivalent to ₹575.00.

Although I don’t have the SBI Cashback card, the AU LIT credit card has not disappointed me at all. It not only gave me substantial cashback but also helped me rack up a ton of reward points. These points can be redeemed for a variety of rewards, making every purchase feel even more worthwhile.

If you’re on the lookout for a credit card that offers great returns and rewards, I highly recommend giving the AU LIT credit card a try. It’s been a game-changer for me!

Attachments