Chill_Odia_Guy

TF Buzz

Hi, Technofino Folks

First of all a big applauds to RBI Ombudsman. 🫡🙏

It all started when I decided to check my CIBIL score through the BankBazaar app, a routine step to keep track of my financial health. Everything seemed fine until I pulled up my full CIBIL report a little later. That’s when I spotted it—an enquiry dated 15th August 2024 for a credit card I never applied for. My first reaction was confusion. I hadn’t requested any credit card, so how did this enquiry end up on my report?

Then it hit me. A few days after checking my score on the app, I’d received a call from someone claiming to be an agent from RBL Bank. They were aggressively pitching an RBL Credit Card, going on about its benefits. I listened politely at first, but I was firm—I told them I wasn’t interested and explicitly said no to any application. I thought that was the end of it. Apparently, it wasn’t. Despite my clear refusal, it seemed they had gone ahead and processed an application without my consent, leaving this unauthorized enquiry on my CIBIL report. I was furious. This wasn’t just a clerical error; it felt like a blatant disregard for my wishes.

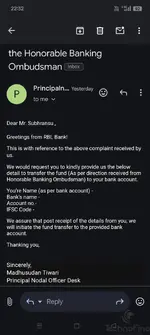

Determined to set things right, I fired off an email to RBL Bank’s customer care, explaining the situation and demanding they remove the enquiry. Their response? A flat denial. They claimed it was a “genuine enquiry” and refused to take any responsibility. I wasn’t surprised—banks often brush off complaints like this—but I wasn’t about to let it slide. So, I escalated the matter to RBL Bank’s Principal Nodal Officer, hoping for a more reasonable resolution. To my disappointment, they echoed the same line: it’s genuine, and it can’t be removed. At this point, I felt stuck. My CIBIL score, something I’d worked hard to maintain, was now tainted by an enquiry I never authorized, and the bank seemed determined to stonewall me.

Refusing to give up, I took the matter to the Reserve Bank of India’s Ombudsman. Filing the complaint was straightforward, but I knew it would take time. The investigation stretched on for three long months, and I’ll admit, there were moments when I wondered if it was worth the effort. But then, things started to turn around. After their review, the RBI Ombudsman ruled in my favor. The first victory came when the unauthorized CIBIL enquiry was finally removed from my report. I checked it myself to confirm—gone, like it never happened. That alone felt like a huge weight off my shoulders.

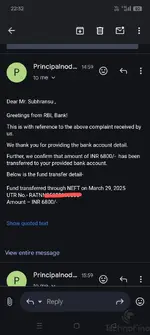

But the story didn’t end there. Yesterday, I received an unexpected email from RBL Bank’s Principal Nodal Officer. This time, it wasn’t a denial—it was a request for my bank details to process a compensation funds transfer. I couldn’t believe it. After months of back-and-forth, they were finally acknowledging their mistake. I sent the details right away, and sure enough, today I checked my account—₹6,800 had been credited to me. It wasn’t just about the money; it was the principle of it all. I’d fought for what was right, and after a long battle with persistence and a little help from the RBI Ombudsman, I’d won.

₹6,800= 68 days X per day ₹100

Justice, it seems, does come—sometimes with a three-month wait and a ₹6,800 cherry on top 🫠.

First of all a big applauds to RBI Ombudsman. 🫡🙏

It all started when I decided to check my CIBIL score through the BankBazaar app, a routine step to keep track of my financial health. Everything seemed fine until I pulled up my full CIBIL report a little later. That’s when I spotted it—an enquiry dated 15th August 2024 for a credit card I never applied for. My first reaction was confusion. I hadn’t requested any credit card, so how did this enquiry end up on my report?

Then it hit me. A few days after checking my score on the app, I’d received a call from someone claiming to be an agent from RBL Bank. They were aggressively pitching an RBL Credit Card, going on about its benefits. I listened politely at first, but I was firm—I told them I wasn’t interested and explicitly said no to any application. I thought that was the end of it. Apparently, it wasn’t. Despite my clear refusal, it seemed they had gone ahead and processed an application without my consent, leaving this unauthorized enquiry on my CIBIL report. I was furious. This wasn’t just a clerical error; it felt like a blatant disregard for my wishes.

Determined to set things right, I fired off an email to RBL Bank’s customer care, explaining the situation and demanding they remove the enquiry. Their response? A flat denial. They claimed it was a “genuine enquiry” and refused to take any responsibility. I wasn’t surprised—banks often brush off complaints like this—but I wasn’t about to let it slide. So, I escalated the matter to RBL Bank’s Principal Nodal Officer, hoping for a more reasonable resolution. To my disappointment, they echoed the same line: it’s genuine, and it can’t be removed. At this point, I felt stuck. My CIBIL score, something I’d worked hard to maintain, was now tainted by an enquiry I never authorized, and the bank seemed determined to stonewall me.

Refusing to give up, I took the matter to the Reserve Bank of India’s Ombudsman. Filing the complaint was straightforward, but I knew it would take time. The investigation stretched on for three long months, and I’ll admit, there were moments when I wondered if it was worth the effort. But then, things started to turn around. After their review, the RBI Ombudsman ruled in my favor. The first victory came when the unauthorized CIBIL enquiry was finally removed from my report. I checked it myself to confirm—gone, like it never happened. That alone felt like a huge weight off my shoulders.

But the story didn’t end there. Yesterday, I received an unexpected email from RBL Bank’s Principal Nodal Officer. This time, it wasn’t a denial—it was a request for my bank details to process a compensation funds transfer. I couldn’t believe it. After months of back-and-forth, they were finally acknowledging their mistake. I sent the details right away, and sure enough, today I checked my account—₹6,800 had been credited to me. It wasn’t just about the money; it was the principle of it all. I’d fought for what was right, and after a long battle with persistence and a little help from the RBI Ombudsman, I’d won.

₹6,800= 68 days X per day ₹100

Justice, it seems, does come—sometimes with a three-month wait and a ₹6,800 cherry on top 🫠.

Attachments

-

Screenshot_2025-03-29-22-30-08-21_e307a3f9df9f380ebaf106e1dc980bb6.webp76.6 KB · Views: 45

Screenshot_2025-03-29-22-30-08-21_e307a3f9df9f380ebaf106e1dc980bb6.webp76.6 KB · Views: 45 -

Screenshot_2025-03-29-22-32-30-74_e307a3f9df9f380ebaf106e1dc980bb6.webp53.3 KB · Views: 40

Screenshot_2025-03-29-22-32-30-74_e307a3f9df9f380ebaf106e1dc980bb6.webp53.3 KB · Views: 40 -

Screenshot_2025-03-29-22-33-04-57_e307a3f9df9f380ebaf106e1dc980bb6.webp52.1 KB · Views: 42

Screenshot_2025-03-29-22-33-04-57_e307a3f9df9f380ebaf106e1dc980bb6.webp52.1 KB · Views: 42 -

Screenshot_2025-03-29-22-32-50-42_e307a3f9df9f380ebaf106e1dc980bb6~2.webp48.3 KB · Views: 41

Screenshot_2025-03-29-22-32-50-42_e307a3f9df9f380ebaf106e1dc980bb6~2.webp48.3 KB · Views: 41 -

Screenshot_2025-03-29-22-42-22-66_e307a3f9df9f380ebaf106e1dc980bb6~2.webp47.9 KB · Views: 43

Screenshot_2025-03-29-22-42-22-66_e307a3f9df9f380ebaf106e1dc980bb6~2.webp47.9 KB · Views: 43