Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

-

Hey there! Welcome to TFC! View fewer ads on the website just by signing up on TF Community.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

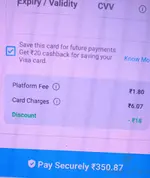

Gpay started 1% inconvenience fee

- Thread starter HumorSimpson

- Start date

- Replies 78

- Views 5K

I will request for cancellation of ace after end of this monthSame here. No usp of ace now

Now Axis ACE can't be used even for gpay utilities

with effective cashback of 3.8% not that worth

with effective cashback of 3.8% not that worth

surojitLaha

TF Ace

Man this is so sad.

I used to pay electricity, water,gas bills using this card 😞

I used to pay electricity, water,gas bills using this card 😞

Bhai, tu 40+ walo ki le raha hai, young people ki le raha hai, non tech savy ki le raha hai? Kiski le raha hai? 😁But problem is 40+ Aged people still use them even they levy convenience fees. Unless you’re tech or fin enthusiast most young people won’t know the alternatives to pay things without any fees & few know how to get something back, every time we pay something. So these Fintech companies mulch on these categories of people

Yes. The clean gpay interface and 5% cashback on ace will be missedMan this is so sad.

I used to pay electricity, water,gas bills using this card 😞

Thanks for sharing

saniruidas

TF Premier

Can I use credit card on Unipay ?I think best option is paying via Unipay Canara Setu, Airtel Or Bank’s Native Apps. But problem is 40+ Aged people still use them even they levy convenience fees. Unless you’re tech or fin enthusiast most young people won’t know the alternatives to pay things without any fees & few know how to get something back, every time we pay something. So these Fintech companies mulch on these categories of people

saniruidas

TF Premier

Now Max 4800 cashback on utility, 600 annual fee 4200 per year profit.Looks like i have to close my axis ace cc

Previous 6000-600= 5400 profit.

1200 less profit 😕.

maheshspanicker

TF Premier

Tata Neu or Amazon, while the fun last there! Tata Neu is already devaluing Neupass, so more should be on the way. Indus Mobile doesn't charge anything, and sometimes gives some small little offers too, but the UI is from the previous century!

Its for those who use ace extensively for ocassional.user it will be 3k annaully over a fee for 590.Now Max 4800 cashback on utility, 600 annual fee 4200 per year profit.

Previous 6000-600= 5400 profit.

1200 less profit 😕.

I got sbi cb 3/4 months back and i already have 7k cb in that....

saniruidas

TF Premier

It's exclusively for utility comes with good benifits, previous devaluation from bank side on others spent 2 to 1.5 % , now devaluation as convenience fee from co branded partner side 1% .Its for those who use ace extensively for ocassional.user it will be 3k annaully over a fee for 590.

I got sbi cb 3/4 months back and i already have 7k cb in that....

Airtel also devaluate monthly 300 to 250.

Cashback card also give cashback in previous without any online marchent restrictions, but then they also restricted utility.

I have paisabazar yes Card it's also give 3% , excludes utility and wallet.

saniruidas

TF Premier

Indie app also gives 50 flat per minimum 500 utility upto 500 per month, but now 25 only.Tata Neu or Amazon, while the fun last there! Tata Neu is already devaluing Neupass, so more should be on the way. Indus Mobile doesn't charge anything, and sometimes gives some small little offers too, but the UI is from the previous century!

I have kotak super account debit card which also gives 5% upto 500 per month. But it's own money 😶

And soon again we will be shifting to cash, as rewards and fees are making themselves equal, so why credit cards use debit cards or upiSoon it will be everywhere with convenience fee or platform fee

Yeah already it's happening with small merchants where they pass the mdr if v use cc. They ask cash or upi upto 50k or net bankingAnd soon again we will be shifting to cash, as rewards and fees are making themselves equal, so why credit cards use debit cards or upi

RAMESH BABU N

TF Legend

CONVENIENCE FEE for them.

INCONVENIENCE FEE for us(ers).

INCONVENIENCE FEE for us(ers).

dexter_greycells

TF Premier

%5 CB - 1% convenience fee is still 4% CB. Don't rush into closing that card.Looks like i have to close my axis ace cc

Also remember it is the industry leader in offering flat and unlimited 1.5% CB (and not RPs) on all offline payments (except the usual exceptions of government, fuel, jewellary, insurance).

I am not rushing. Will do the gimmick of threatening to close the card on next annual fee billing month March'25 and I really don't care even if they close it.%5 CB - 1% convenience fee is still 4% CB. Don't rush into closing that card.

Also remember it is the industry leader in offering flat and unlimited 1.5% CB (and not RPs) on all offline payments (except the usual exceptions of government, fuel, jewellary, insurance).

- 5% CB on bills can be achieved thru sbi cb agv route

- for offline kiwi 2% CB works well.

Similar threads

- Question

- Replies

- 55

- Views

- 8K

- Replies

- 1

- Views

- 523

- Replies

- 10

- Views

- 1K

- Replies

- 33

- Views

- 2K