D

Deleted member 21631

Guest

I have an HDFC Account, where I opted for Overdraft (OD) against FD facility. Unlike most overdraft accounts, HDFC didn't created a separate account, but added the overdraft limit as balance in my regular account, and from there, I can use it without any problem for any payment (also helps maintain MAB, even if actual bank balance is ₹0)

I primarily opened HDFC account for credit card and bank employee said that getting OD against FD will help me get a credit card soon (probably for generating my cibil score).

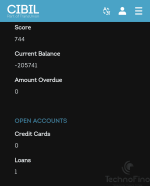

Today, my CIBIL score got generated with 744 score and my credit utilization is 0%. But the problem is, my debt is showing Rs -2,05,741 (yes, in negative). Probably, since I had this extra money in my bank account when HDFC reported to Credit bureaus.

This technically means, I have extra money in my loan account and the Bank owes me money instead of me owing to the Bank

So, my questions are-

1. Will this negative debt that has been reported to credit bureau, impact my credit report badly?

2. Is this safe? Should i report to Cibil or hdfc bank?

3. Is my CIBIL score bad, since its 744, in CIBIL app, its showing as 2nd bottom on credit score ranking? Can anyone tell me what their score was when it was generated for the first time?

4. Will this overdraft facility affect me in getting a pre-approved Credit card from the bank, as its a loan. Currently, i am maintaining 4.3L in this account.

5. If I can get a pre-approved credit card, should i keep this overdraft facility on?

Please answer them and thank you for reading it")

I primarily opened HDFC account for credit card and bank employee said that getting OD against FD will help me get a credit card soon (probably for generating my cibil score).

Today, my CIBIL score got generated with 744 score and my credit utilization is 0%. But the problem is, my debt is showing Rs -2,05,741 (yes, in negative). Probably, since I had this extra money in my bank account when HDFC reported to Credit bureaus.

This technically means, I have extra money in my loan account and the Bank owes me money instead of me owing to the Bank

So, my questions are-

1. Will this negative debt that has been reported to credit bureau, impact my credit report badly?

2. Is this safe? Should i report to Cibil or hdfc bank?

3. Is my CIBIL score bad, since its 744, in CIBIL app, its showing as 2nd bottom on credit score ranking? Can anyone tell me what their score was when it was generated for the first time?

4. Will this overdraft facility affect me in getting a pre-approved Credit card from the bank, as its a loan. Currently, i am maintaining 4.3L in this account.

5. If I can get a pre-approved credit card, should i keep this overdraft facility on?

Please answer them and thank you for reading it

Attachments

Last edited by a moderator:

.

.