Navigation

Install the app

How to install the app on iOS

Follow along with the video below to see how to install our site as a web app on your home screen.

Note: This feature may not be available in some browsers.

More options

Style variation

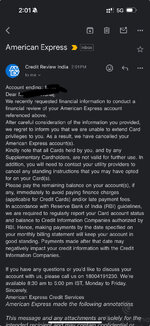

-

Hey there! Welcome to TFC! View fewer ads on the website just by signing up on TF Community.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

What can be done, as Amex is cancelling my cards

- Thread starter Heisenberg37

- Start date

- Replies 90

- Views 9K

You are right I deleted that part.Why begging for reputation points in almost every alternate post Sir? If you are good at something, people will anyways appreciate you.

It is not at all important

Congratulations! then you do not need any Amex card.I already got Infinia and biz black at 19

so be happy and move on

I do 1500*4 nps, for a year 50k benchmark can be achieved. 15₹ surcharge extra for paying through any creditcard.How much reward we get for paying nps payments of Rs50000 for one financial year , and also nps payments allow credit card with a fee, does amex cards support? Please provide more info on this , I would like to save some money on nps payments

Sometimes I do 1500*2 or 1500*3, depends on my monthly spends..

I dont think you can convince AMEX to let you keep these cards. Maybe you can negotiate to let them use your points (redeem or transfer out) - but if they believe points were earned in contravention to their MITC, then youve lost those too.Hi guys

As in previous post i shared my experience of horrible FR.

Now that they are cancelling my cards is there anything i can do to convince them to keep them.

And for example they cancelled my cards when can I reapply again?

Next step is to understand are you permanently banned (PAN BLOCK) with Amex or can you reapply (if you are still interested) after a break.

its 0.70% if you use CC (Amex works) for Tier 1 investments + 18% GST so comes to about 0.82%.I do 1500*4 nps, for a year 50k benchmark can be achieved. 15₹ surcharge extra for paying through any creditcard.

Sometimes I do 1500*2 or 1500*3, depends on my monthly spends..

Small correction. It's 0.75% + gst = 0.885%its 0.70% if you use CC (Amex works) for Tier 1 investments + 18% GST so comes to about 0.82%.

ahha thanks. havent paid via CC in last 3-4 months hence forgot the exact amount!Small correction. It's 0.75% + gst = 0.885%

That why amex cancelled. itr of 12.5L n spend are 3x only cause you asked for more le.I spent around 40 L from all of my cards in 1y3 months

Payment history was good

Cibil 779

gauravsuthar

TF Buzz

Thread is not available.I have taken the trouble to made a thread on cards giving over 10% return.

Thread 'Cards giving 10% return or more' https://www.technofino.in/community/threads/cards-giving-10-return-or-more.25667/

you need to be a select or higher i think to get access.. so earn more points by being more active!Thread is not available.

I already posted the list in this thread. Look above at the post number 37Thread is not available.

The answers to your 2 questions are --Hi guys

As in previous post i shared my experience of horrible FR.

Now that they are cancelling my cards is there anything i can do to convince them to keep them.

And for example they cancelled my cards when can I reapply again?

1. You cannot convince them to reinstate your cards, after seeing what they have written.

2. You cannot re-apply again if they have permanently blocked your PAN

But most importantly, the solution to your problem is--

3. You should not be concerned about having or not having a card which gives you a lot of hassle to earn merely 4 to 5% return (after deducting the renewal fees).

Remember I purposely and purposefully closed MRCC, even though I was getting 16.67% higher return than everyone is getting now. (I had it for 4 years before the devaluation)

See my post number 37 mentioning 10 cards which are so much better and give over 10% return

you can and should choose from these better cards and move on 🤠

Kindly mark this as your solution, thanks 🙏

Last edited:

popkorn

TF Buzz

correctAll Amex cards are useless and complicated. All thess monthly tasks of 1000x6, 1500x4, 20000, 2x reward multiplier, buying vouchers, requesting for fee waivers every time etc. are completely not worth. Too much hassles and headache. Better to have a cashback card like SBI cashback that gives real 5% cashback on online transactions. You will not miss Amex a single day!!

your fate is like that . What others to do further?I agree . For most people this point is true including me but there can also be instances where people who are high earners and spenders can milk the card properly and take full advantage. But the fact is that according to many amex card holders the services from last two years has deteriorated so much that it doesn't feel premium any more. As Amex is mostly held by individuals upwards of 10 crore net worth who don't care about 5% petty cashback like we do.

santoshraut

TF Buzz

Let it go forever. It's not worth it. Acceptability of AmEx card is very low, and they are planning to devaluate it soon like other credit cards. I recently closed my MRCC and PT. I am very happy with my Axis Atlas, HDFC Infinia, SBI Club Vistara, AU Zenith Plus, and a few more...Hi guys

As in previous post i shared my experience of horrible FR.

Now that they are cancelling my cards is there anything i can do to convince them to keep them.

And for example they cancelled my cards when can I reapply again?

Return on amex is obviously bad if you want to redeem for anything other than travel.All this Hassel just to get 4.43% and 5.66%

How about using SBI CB or hdfc millennia and buy Amazon gv to get 5% instead 😂

Even within travel it's great if you opt for marriot. I'm easily able to get more than inr 1 value of each amex point by using them for marriot stays. Recently booked westin Rishikesh for 18k points per night when price on mmt was 40k per night so that's a value more than inr 2 per point. However, we can keep the value at inr 1 for simplicity.

Coming to earning points.

While spending 20k monthly on mmrc purely on gftyr, I am able to get 2k bonus reward points plus 800 points on spending that amount through 2x multiplier applicable on gfytr. In total 2.8k points every month so that's 14% return for me. Mmrc is ltf for me but it's full fee is waived off anyway if you spend 1.5L in a year which will happen for anyone who is spending 20k every month.

Even if someone does no spends on gyftr, they will get a return of 12% which is great

Westin Rishikesh is outlier. Recently they have also changed points requirement to 25K per night. Leaving this use case aside, do you think you can consistently extract 1Rs per MR point in the future?Return on amex is obviously bad if you want to redeem for anything other than travel.

Even within travel it's great if you opt for marriot. I'm easily able to get more than inr 1 value of each amex point by using them for marriot stays. Recently booked westin Rishikesh for 18k points per night when price on mmt was 40k per night so that's a value more than inr 2 per point. However, we can keep the value at inr 1 for simplicity.

Coming to earning points.

While spending 20k monthly on mmrc purely on gftyr, I am able to get 2k bonus reward points plus 800 points on spending that amount through 2x multiplier applicable on gfytr. In total 2.8k points every month so that's 14% return for me. Mmrc is ltf for me but it's full fee is waived off anyway if you spend 1.5L in a year which will happen for anyone who is spending 20k every month.

Even if someone does no spends on gyftr, they will get a return of 12% which is great

In Los Angeles near Hollywood boulevard, right now I can see a 3 star Marriott hotel for 88000 Marriott points for two nights.Return on amex is obviously bad if you want to redeem for anything other than travel.

Even within travel it's great if you opt for marriot. I'm easily able to get more than inr 1 value of each amex point by using them for marriot stays. Recently booked westin Rishikesh for 18k points per night when price on mmt was 40k per night so that's a value more than inr 2 per point. However, we can keep the value at inr 1 for simplicity.

Coming to earning points.

While spending 20k monthly on mmrc purely on gftyr, I am able to get 2k bonus reward points plus 800 points on spending that amount through 2x multiplier applicable on gfytr. In total 2.8k points every month so that's 14% return for me. Mmrc is ltf for me but it's full fee is waived off anyway if you spend 1.5L in a year which will happen for anyone who is spending 20k every month.

Even if someone does no spends on gyftr, they will get a return of 12% which is great

Whereas a similar 3 star hotel in the same location I can get at a discounted revenue price of Rs 17850 for 2 nights on Agoda, including all taxes and 5% Agoda forex markup.

This specially discounted rate is only if you go through Google hotels and not directly on the Agoda website

Last edited:

Now able to open the link.I already posted the list in this thread. Look above at the post number 37

Why do you need Amex at all when there are so many better cards available giving much higher returns without any hassle /trouble of doing 4 x 1500 and 6 x 1000 every month?Now able to open the link.

Not to mention the very poor acceptance of Amex cards in India.

Why do you think Amex was paying all its card holders to get new members?

That too a HUGE 12000 points for each and every new member!!

These are some cards giving 10% or more on select categories--

1. Axis Magnus Burgundy

30% on Eazydiner (900--1000 on 3000--3333)

24% on Grabdeals (upto 16666/mth)

24% on Traveledge (upto 2 lacs/mth)

2. HDFC Infinia

15.55% (Smartbuy 5x upto 112500)

31.10% (Smartbuy 10x upto 49950)

3. Axis Atlas

10% on Traveledge, direct hotels and direct airlines, no cap

4. Axis Airtel (on Airtel Thanks app)

25% on Airtel (max.250 on 1000)

10% on utility bills (max.250 on 2500)

10% on Swiggy, Zomato, BB (max.500 on 5000)

5. HDFC Swiggy 10% on Swiggy delivery

6. AU Lit

5% grocery/apparel + 5+1% bonus + 2% online/offline (on 10000/mth)

7. HDFC Biz Black

16.66% on tax payment (50000 to 56250 spend per month)

8. HSBC Cashback

10% on dining, groceries and food delivery, (max.1000 on 10000) (only for salaried employees)

9. IndusInd exclusive/select debit card

20% discount (max 500 on 2500) on big basket between 1st to 25th of every month.

10. Rupay debit card

20% discount on mobile recharge on Amazon every Friday (max 100 on 500)

Kindly mark this as your solution thanks 🙏

Last edited:

Similar threads

- Replies

- 127

- Views

- 13K

- Question

- Replies

- 99

- Views

- 9K

- Replies

- 46

- Views

- 2K

- Replies

- 6

- Views

- 718