The number of credit card users in the country has boomed exponentially over the last few years, and with it, so have cases of mis-selling credit cards. One of the most common tricks is when bank employees promise you a lifetime free credit card, but you end up getting a paid one instead. But that’s just the tip of the iceberg—if you dig a little deeper, you'll see there are several sneaky tactics bank employees use to push credit cards or other banking products onto customers.

Let's explore some common ways bank employees mis-sell products:

Key things every banking customer should know:

My personal experience: In 2020, HDFC Bank upgraded my credit card from Regalia First to Regalia and eventually to Infinia, with a limit increase from ₹1 lakh to ₹10.13 lakh. I was a "Classic Banking" customer at the time and later upgraded to "Imperia Banking", but I haven't received any limit enhancement offers since. On the other hand, I had a Pioneer relationship with IndusInd Bank, requested a lifetime free Heritage Metal Card, and they approved it even though my balance was lower than required for pioneer. Similarly, YES Bank upgraded my credit card from YES First Exclusive to YES Private based on my overall net worth, while I maintained a zero-balance account with them.

What to do if you've become a victim of mis-selling:

What we can do: We can raise awareness by sharing such experiences on social media and informing other customers to help them avoid these traps.

Here are a few real cases I found in the "Banking Complaint" section of the TF Community. If you dig deeper, you’ll find countless similar cases with every bank:

But why do bank employees mis-sell products? It's usually due to the pressure of meeting sales targets or the high commissions they receive for selling certain products. It's your responsibility not to fall into these traps.

I've seen many people get emotionally attached to their bankers. While it's not a bad thing to be kind, based on my experience, you should be cautious with your banker. They work for their bank and focus on earning money for the bank. They generally don't care much about your financial well-being or interests.

I've mentioned this before: Relationship Managers (RMs) are assigned to you by banks to generate profit. They're not qualified investment bankers, just sales agents who speak good English and are skilled in sales tactics. Have you ever seen a bank assign an RM to a lower-tier account? No, because they know that if you don't maintain a significant balance, it wouldn't be worth their time.

Let's explore some common ways bank employees mis-sell products:

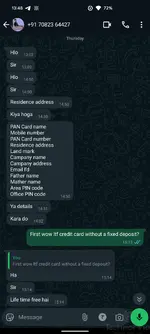

- False promises of lifetime free cards: Bank employees contact customers and promise a lifetime free (LTF) credit card. After approval, the customer finds out they've been issued a paid credit card.

- High variant card with account opening: Employees promise a higher variant credit card for free (LTF) but ask the customer to open a higher variant bank account with a high initial deposit. Sometimes, they even suggest opening similar accounts for family members and creating a "family banking" group.

- Credit limit linked to account opening: Employees promise a high credit limit on the credit card, but only if the customer opens a higher variant bank account and maintains a large balance for a while.

- Linking investments to credit card approval: Employees ask customers to invest in ULIPs or other insurance products in exchange for credit card approval or an upgrade.

Key things every banking customer should know:

- Bank employees cannot approve your credit card. Banks have dedicated underwriting teams that assess your credit profile and make decisions.

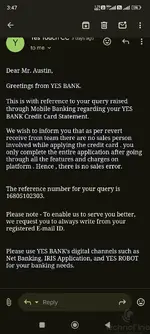

- WhatsApp chats or phone call recordings are not valid proof. If a banker promises you something like a lifetime free credit card, ensure you get it in writing via email from their official email ID.

- In most cases, opening a bank account or maintaining a high balance does not affect your credit card approval process. If a bank employee insists on this, ask for confirmation in writing via email. In 99.99% of cases, they won't be able to provide this because it's not true.

My personal experience: In 2020, HDFC Bank upgraded my credit card from Regalia First to Regalia and eventually to Infinia, with a limit increase from ₹1 lakh to ₹10.13 lakh. I was a "Classic Banking" customer at the time and later upgraded to "Imperia Banking", but I haven't received any limit enhancement offers since. On the other hand, I had a Pioneer relationship with IndusInd Bank, requested a lifetime free Heritage Metal Card, and they approved it even though my balance was lower than required for pioneer. Similarly, YES Bank upgraded my credit card from YES First Exclusive to YES Private based on my overall net worth, while I maintained a zero-balance account with them.

What to do if you've become a victim of mis-selling:

- Raise a complaint with the bank's grievance redressal team.

- If the issue isn't resolved within 30 days, escalate the matter to the RBI Banking Ombudsman.

What we can do: We can raise awareness by sharing such experiences on social media and informing other customers to help them avoid these traps.

Here are a few real cases I found in the "Banking Complaint" section of the TF Community. If you dig deeper, you’ll find countless similar cases with every bank:

- RBL Card Mis-Selling by Branch Staff

- RBL ShopRite Card Mis-Selling - Need Help

- Kotak Mis-Selling, RBI Ombudsman

- AUSFB - Credit Card Mis-Selling by Branch Employee

- Standard Chartered Bank Mis-Sold Savings Account and Credit Card

- HDFC Bank Mis-Selling Insurance Policies in Exchange for Infinia Credit Card

- HDFC Mis-Selling SWIGGY HDFC Credit Card

- Mis-Selling SBI Card Through BankBazaar

But why do bank employees mis-sell products? It's usually due to the pressure of meeting sales targets or the high commissions they receive for selling certain products. It's your responsibility not to fall into these traps.

I've seen many people get emotionally attached to their bankers. While it's not a bad thing to be kind, based on my experience, you should be cautious with your banker. They work for their bank and focus on earning money for the bank. They generally don't care much about your financial well-being or interests.

I've mentioned this before: Relationship Managers (RMs) are assigned to you by banks to generate profit. They're not qualified investment bankers, just sales agents who speak good English and are skilled in sales tactics. Have you ever seen a bank assign an RM to a lower-tier account? No, because they know that if you don't maintain a significant balance, it wouldn't be worth their time.